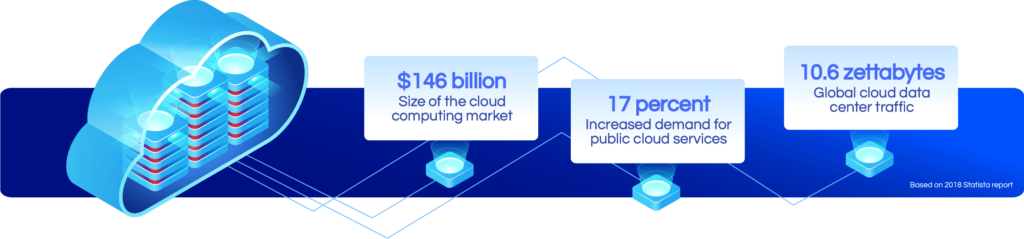

Because of its prevalence, most people already know what this is, but put simply, the cloud allows an internet user to access a third-party computing resource located in almost an endless network of interconnected servers that allow you to run your computer’s applications over the internet without having to buy, install or manage your own servers.

What this means is you could run your firm’s IT operations with nothing more than a browser and internet connection. By using the cloud, firms of all sizes can reduce IT costs, manage data storage needs more effectively, and improve staff flexibility. In a short amount of time, the cloud has emerged as one of the most meaningful innovations in technology.

The cloud symbol was first used to represent the public telephone systems on our dial-ups and since the original basis of the internet was through dial-up modems, that symbol has been used and now represents what we know of today as “the cloud.” Before we go on, it is important to note that when we say “client-server,” the word “client” does not refer to your customer. Depending on your role, this word means two different things (depending on if you’re on the IT team or an attorney.) The word “client” to an IT person means a device used by one person at a time to access the internet. Essentially it is just an access point, whether it’s a smartphone, tablet, PC, you name it. These access points (or clients), and central servers which supply applications and data, are shared amongst several clients and can be accessed at any one time. So when you sign in to Gmail, or anywhere on the internet, you’re not the only person at that exact moment who can gain access. Thousands, if not millions of people could access their Gmail account at the same time through their own client-server.

Characteristics of the Cloud

Let’s take a look at the five essential characteristics of the cloud:

On-demand self-service

Broad network access

Resource pooling

Rapid elasticity

Measured service

On-demand self-service

On-demand service essentially means you order what you want when you want it. You can unilaterally make such provisions either regarding server settings or network storage without the need for any interaction from the provider’s IT administrator. Further examples of such resources include storage, processing, memory, network bandwidth, and virtual machines.

Broad network access

Broad network access means you have access to your data over the standard network through client platforms such as your smartphone, PC, or laptop.

Resource pooling

Resource pooling simply means that providers serve multiple customers, with provisional and scalable services. These services can be adjusted to suit each customer’s needs without any changes being apparent to the customer or end-user. When you access a server on the internet, it’s not only your information on that server, there is other people’s information as well. Sometimes there may just be one server for 50 different people and sometimes it could even be located overseas. As attorneys, this is incredibly important to be aware of. Many firms will just sign up or pay for cloud services and have no idea where their actual data is being stored, or who it’s being stored with. Sometimes it’s because they don’t care, and other times it’s because they don’t know to ask. So make sure you ask your vendor this question!

Rapid elasticity

Rapid elasticity allows users to automatically request additional space in the cloud or other types of services. ... In a sense, cloud resources appear to be infinite or automatically available. That's very different from older systems, where the limits of storage or memory were immediately visible to a user. Compared to on-premise servers, this process is significantly easier and more convenient.

Measured service

Resource usage can be monitored, controlled, and reported. This provides transparency for both the provider and the consumer of the service. Your firm can actually get insight into the performance of your network with statistics that monitor your usage.

Will the Cloud Save my Firm Money?

The first question that many firms ask cloud providers is, “how much will it cost?” This is a logical question, but the price range varies so drastically, that it makes more sense to narrow down specific goals and aspects of your firm. Let’s take a look.

Take a look at the chart below. The first thing you need to consider is the upfront expenditure. Let’s look at the on-premise category first. A good quality single server with no redundancy can run anywhere from $3,500-$8,000 if you’re going low end. A decent, middle-of-the-road server will land you north of $10,000. With that, you will need a backup system, which incorporates both software and hardware which could easily tack on another $2,000+. Next, you will want a quality APC battery or locate your system in a colo-data center to protect all of this valuable equipment. Following that line item is your server licensing. This is not per physical server, but per virtual server which typically runs inside of one box. Traditionally, you will be running an active directory, a file server, and a database server. Best practices dictate you separate these roles into multiple servers, but you could combine some of these roles into two servers, which is where you get the $1,900. Next are your user licenses or your client access licenses. This is required for each person who needs access to the server. If they run slightly over $40, and you have 15 people at your firm, you’re looking at about $840. Another expense is your Microsoft SQL licenses which almost every on-premise case management system requires. You can pay for this by the processing core, or by the user, but either way, it comes out to about the same. Finally, There will definitely be implementation fees to get this all together and have your firm up and running. With the going IT rate, you’re looking at about $5,000 of total labor.

The next two columns are much more simplistic. All the listed services are either included in a private cloud or are not applicable. With the cloud, you will still have a labor fee that will either be due upfront or spread out with payments over a designated period of time. For web applications, if you’re considering a change, this will oftentimes require the assistance of a third-party consulting firm.

Expenses

On-Premise Servers

Cloud

Web Applications

Server(s) Hardware

$5,500

Included

N/A

Backup Solution

$2,000

Included

N/A

APC Battery

$1,500

Included

N/A

Microsoft Server Licensing ($950/ea.)

$1,900

Included

N/A

Microsoft User Licenses ($42/ea.)

$840

Included

N/A

Microsoft SQL Licenses ($209/ea.)

$4,180

Included

N/A

Terminal Server Licenses ($133/ea.)

N/A

Included

N/A

Setup Fee

$5,000

$4,425

$7,500

Total Up-Front Cost

$20,920

$4,425

$7,500

Now that we have talked about the upfront costs, let’s look at some of the common monthly expenditures:

Expenses

On-Premise Servers

Cloud

Web Applications

Server Maintenance ($200-$350/ea.)

$5,500

Included

N/A

User Support + Anti-Virus ($49/user)

$735

Included

$735

Offsite Backup (25-75 cents/gig)

$100

Included

N/A

Remote Access (GoToMyPC: $30/user)

$450

N/A

N/A

Cloud Storage ($0-$50/user)

N/A

Included

$105

Total Monthly Costs

$6,785

$2,085

$840

The first line item is your server maintenance. If you have a server, you will want to make sure that it is properly maintained, monitored, secured, and audited on a routine basis. This is especially critical with the security threats we face today. Assuming you’re running 2-3 virtual servers, you’re looking at about $500.

User support entails the support for each computer, anti-virus work, print capabilities, and general network support. The average spend for this is about $49 per user, per month. Some firms will have an in-house IT team, others will outsource the help. The former is quite costly as you’re salarying these additional team members, but outsourcing your support can be tricky if you need immediate assistance. For web applications, keep in mind that if you can eliminate all of your servers, this cost will remain, and in some cases, this cost may increase as computer management becomes increasingly difficult with no server to help automate management.

Next is the offsite backup category, this is native to almost all cloud solutions, whereas on-premise servers need to be backed up nightly. Be warned that if you are not backing up your data, you risk losing it in a crash. Paying for such solutions varies drastically in price, if you’re looking for a full backup and disaster recovery solution, you could be looking at thousands per month. For the sake of our example, we took the very basic backup system which typically charges between 25-75 cents/gig.

Now, looking at remote access, this also runs natively to any cloud-based solution. If you have an on-premise option, you can get a dedicated terminal or Citrix server. This would add significant spending to the upfront and server maintenance columns. Since we’re considering a 15-user law office, chances are, they’re using RDP over VPN directly to their desktop, or more commonly, a GoToMyPC or log me in a type of solution.

For storage, most firms with on-premise servers are using their file server which could be your S drive or your T drive (for example). Additional costs here come from when your file server runs out of space or there’s a server malfunction or breach.

Everything we just mentioned encompasses the average base cost for each solution. Each service provider is different, and fees will vary depending on what your firm chooses to adopt vs. waive.

Ready to see how cloud-based Centerbase cuts costs and raises your revenues?

The chart below looks at some features that cannot be quantified mathematically, but they hold immense value.

Each firm has to evaluate which of these intangible assets are most critical, and which are considered to be more of a luxury. Consider things like mobile access and liability. Do you have plans to geographically expand your firm? Do you want your staff to be connected with centralized access to the same data? Do your due diligence before signing on the dotted line.

Ultimately, all of these intangibles should help you evaluate whether your firm should pursue cloud, on-prem, or web application services, so don’t take them lightly!

Intangibles

On-Premise Servers

Cloud

Web Applications

Mobile

Limited

Robust

Medium-Robust

Security

Low-Medium

Robust

Robust

Reliability

Low-Medium

Robust

Robust

Scalability

Limited

Flexible

Flexible

Centralization

Centralized

Centralized

Fragmented

Liability

Risky

Limited

Limited

Software Robustness

Robust

Robust

Limited

Support

General

Legal-Centric

Fragmented

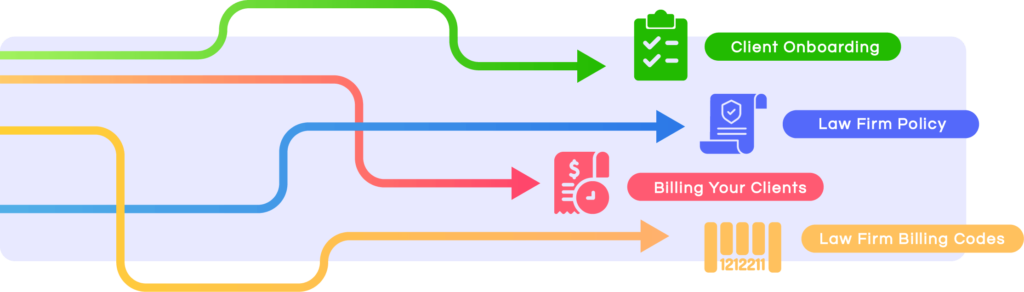

The legal billing process can be a challenge for every law firm, but it doesn’t have to be. A combination of the right policies, procedures, and technology can be used to stay on top of attorney time and make the billing process efficient and accurate.

Software that encompasses both practice management and time and billing in one platform is an effective way to keep everyone on the same page and meet your clients’ needs. Use your firm’s legal software and good policies and procedures to:

Set up a client onboarding process that is consistent, seamless, and gives your new client confidence in your firm;

Ensure that all of your attorneys and paralegals are following your firm’s protocols so that you use your billing process to communicate value to your clients with accurate time entries, and make the end-of-month billing process efficient and painless.

Client Onboarding

Your law firm’s billing protocol should start with your client onboarding process. Using your practice management software, create a standardized client intake form that captures all of the necessary information upfront. It is important to set appropriate expectations from the start. Once the client and attorney have agreed on a budget and a billing rate, an engagement letter should be sent to the client for signature to ensure all parties have acknowledged in writing what is included in the representation and what the fees will be for that scope of work. Best practice steps include:

Attorney speaks with the client and comes to an agreement on the scope of work and cost.

Assistant sends engagement letter (EL) to client and calendars a task in the practice management system to ensure a signed EL is returned by the client.

Assistant notifies attorney when signed EL is returned so that work may commence. (It is risky to start work before that signature comes back – clients sometimes change their minds!)

Law Firm Billing Policy

Once the client has been engaged and you have received the returned EL (and a retainer payment if one was requested), it is time to get to work. Your firm should have protocols in place that set clear expectations for your attorneys with regard to posting their time to your time and billing system promptly. Research shows that up to 30% of fees are lost when time is not captured concurrently. Best practice steps for a firm billing policy include:

Create and communicate a timekeeping policy and ensure it is supported by leadership.

Give proper training, including do’s and don’ts/time entry examples for your practice. Time entries should be succinct with enough information to show value without being overly wordy.

Require concurrent timekeeping.

Use a user-friendly time and billing program. A cloud-based system will help your attorneys to capture time no matter where they are.

Teach your attorneys to use your billing system’s timer.

Provide your timekeepers with weekly MTD reports on their posted time to keep them from falling behind.

Provide appropriate non-billable task codes for capturing tasks such as business development, internal meetings, training, etc. so that everyone can see where their non-billable time is going.

Law Firm Billing Codes

Some clients require LEDES e-billing, and it is important that your time and billing software support this requirement. The American Bar Association has created a Uniform Task-Based Management System (UTBMS) that allows large clients (typically insurance companies, but sometimes large corporations), to track the work their law firms are performing by task. The Litigation Code Set is most often used, but there are other sets for Counseling, Project, and Bankruptcy Codes as well.

For your clients who use the LEDES e-billing practice, it is important that your time entries are drafted very carefully. Your invoices will be reviewed by a third-party administrator who is looking for anything that appears to have the potential of being an uncovered activity. Best practice steps for LEDES e-billing include:

Ensure you use the UTBMS task codes for your time entries. You may require your timekeepers to enter these themselves, or you may have a billing clerk handle the entry of all of the appropriate codes when it is time to review pre-bills.

Train your paralegals on the importance of very accurate billing descriptions that do not sound clerical in nature.

Train your attorneys on the importance of very accurate billing descriptions that do not give the appearance of being a task a paralegal could have performed.

No block billing. Zero. If you receive an email and you respond to an email, it requires two separate entries.

Someone in your billing department should review these pre-bills carefully prior to submittal to try to avoid time entries from being rejected.

If you do receive a rejection for time entries, you can appeal the decision with more information, but it is much easier and more efficient to avoid this process by getting things right from the start.

Be sure to read your client’s billing instructions carefully. Each client will have different billing guidelines. Many will not pay for what they consider to be operating expenses, such as online research, postage, and photocopies.

Billing Your Client

When it comes time to send your clients their invoices, if your attorneys and paralegals have kept accurate, concurrent time and they have followed your firm protocols for time entries, the billing process should be painless. Your time and billing software should allow you to have a billing template that is specific to your firm. Some software will allow you to review invoices in the pre-bill state within the system, where partners can review the pre-bills, forward questions to timekeepers on their time entries, and release the pre-bills to be invoiced when questions have been answered. Best practice steps in the billing process include:

Firm manager reviews pre-bills for accuracy in billing rates, client disbursements, and overall appearance.

Responsible partner reviews pre-bills to ensure time entries are accurate and communicate value to the client.

Firm manager or billing clerk processes pre-bills using firm’s billing template to submit invoices to clients.

Take a Breather (Until Next Month!)

The monthly law firm billing process does not have to be painful. With the right technology and a few policies and procedures in place, your process can run smoothly and you can have accurate invoices that show value your clients are willing to pay for.

In 2021, whether you realize it or not, you’re a “mobile” lawyer. The digitalization of the world we live in has made the proliferation of cellphones and on-the-go devices an undeniable part of our everyday routine.

Did you know that as of 4 years ago, nearly 100% of lawyers were using mobile computing tools for at least some aspect of their practice? So now, it isn’t “nearly,” it is a resounding “everybody.” Everyone has a cell phone and everyone uses it both for personal and professional reasons. We are all working in a mobile world these days and the expectation is that we will have access to our information from wherever we are.

The first time many of us remember seeing a mobile device was in the 1987 action flick, Lethal Weapon. It was this massive square hunk of material connected to this even clunkier receiver that Roger Murtaugh lugged around across LA. Since then, we have seen this evolution from our Nokia candy-bar phones to flip phones and Blackberrys. But now many decades later, 80% of attorneys are using these beautiful slabs of indestructible (so they say) glass called iPhones. We think of these devices as mobile phones that happen to do a few other things on top of making calls and sending texts. But, think about all the things your phone has replaced… we’re talking about email, calendaring, camera, books, TV, games, tickets, GPS the list goes on and on.

What you should be taking away from this is the fact that these devices are no longer small, single-serving phones. They are an entire personal computer. Our phones have become the primary PC that most of us use on a constant basis. Of course, we have desktops and laptops, but these sleeker and portable devices are one of the first places we go to when we wake up and the last thing we put down at night. There is no other piece of technology that we own that is so pervasive in our lives.

You may be asking yourself, so what? Isn’t technology supposed to grow and evolve and improve? And obviously, the answer to that is yes, but what hasn’t evolved with the changes in our technology is how we protect the information we interact with. Right now, our mobile devices are still thought of as “phones.” And how we protect and monitor them reflects that. However, we go to much greater lengths to protect our servers and our computers. But think about what we just talked about. Our phones are our computers too, and they must be protected as diligently.

Duty of Competence

A few years ago the ABA President started a Commission where they were tasked with looking at whether or not they should make any changes to the Model Rules of Professional Conduct to address the idea that technology today affects nearly every aspect of our legal work. This includes how we store information, how we communicate with clients, how we conduct discovery, and so on.

The ABA went on further to say that: “In the past, lawyers communicated with clients by telephone, in person, by facsimile, but today, lawyers communicate with clients electronically. Confidential information is stored on mobile devices, including the cloud.” Ultimately, this Commission determined that there needed to be some changes to the Model Rules of Professional Conduct. These changes emphasized that it is part of a lawyer’s general and ethical duty to remain competent in a digital age.

To be more specific, this change was most reflected in Rule 1.1- The General Duty of Competence. There was no major change to this actual rule, but an addition was made to comment 8. The section opener remained the same: “To maintain the requisite knowledge and skill, a lawyer should keep abreast of changes in the law and its practice, including the benefits and risks associated with relevant technology..” This means the technology you use to run your practice. Every firm uses technology in its practice. Whether it’s simply Microsoft Word or a billing software, everyone uses something. We hear some firms say that they only care about the states that are relevant to their operations. Currently, 38 states have adopted this revised Duty of Competence.

Application to Your Daily Practice

So what does this mean when it applies to your daily practice, from a practical level? We typically think of technology competence as protecting our client’s information, but if we dig deeper, we will find that it incorporates these 5 things:

Safeguarding client information and remaining up to date on the various risks and benefits associated with relevant technologies

eDiscovery, including the preservation, review, and production of ESI (This includes social media discovery, which opens a Pandora’s box of ethical issues)

The technology that lawyers use to run their practices (This can include communication and file share technologies, software for document generation, electronic calendaring, and docketing tools. Many of these applications store information in the cloud so this realm includes competence with cloud-based operations)

Understanding the technology used by your clients to design or manufacture products or to offer particular services

The technology used to present information in the courtroom

Let’s dig a little deeper into points 1 and 3…

What does that mean exactly when we say the benefits and risks associated with relevant technologies?

The Benefits

The benefits of mobile devices are incredible. That is an undisputed statement. We can now get our work done anywhere at any time, and now with the necessity to work remotely, this capability has become even more critical. Speed is also another advantage, we can communicate so much faster with both our internal teams and our clients without missing a beat. And if you’re on a cloud-based practice management system, you can truly access any file, any document, anything about all your matters from wherever you are all from your phone.

The Risks

The first and most obvious risk with mobile devices is the chance of either misplacing, losing, damaging, or getting it stolen. The question isn’t if this will happen, it is when it will happen.

It was reported that women are 42% more likely to have their phone stolen while men are 57% more likely to drop their phone in the toilet. And a recent study released from Kensington revealed the costs associated with the loss or theft is far greater than the cost of the device itself, thanks to lost productivity, the loss of intellectual property, data breaches, and legal fees.

Regardless of whether your phone is stolen or lost, there are a lot of associated risks that come with that. But no application on our phones runs as much risk as our email does. Today, we use email to communicate with our clients and colleagues. Today we use email as the primary means to transport files and documents. If someone was able to access your phone, they may not be a hacker, but they know what the mail app looks like. If they are able to open this app, they will have complete and unfettered access to the most confidential and sensitive information that has been entrusted to you. And it isn’t just the messages or communications, it’s the attachments! Even with eDiscovery, a vast number of loose files (word documents, pdf, photos), are attached and sent via email.

Ultimately, this is the inherent risk involved.

So what can we do? Let’s find out...

Best Practices to Protect Your Mobile Information

No one expects you to be a mobile security expert. Things happen and the best you can do is be prepared and stay informed of the things you can do. So, with this in mind, when you’re using a mobile device, be aware of these things:

Wifi- Open public wifi networks, as convenient and accessible as they are, pose risks. For one, your data can be accessed by third parties, hackers, or the stranger sitting next to you. It’s also important to note that this person or entity doesn’t have to be physically sitting near you, they could be anywhere in the vicinity to ascertain your data as it flows across the router and across the network.

GPS- The GPS feature in our phones today is unprecedented. However, there is another setting in your phone called “significant locations,” where you can access a list of all the major cities and places you have been to over the course of a few weeks. This feature is automatically enabled, so it is important you are aware of it so you can disable it if you so choose. If someone gained access to inside your phone, they would be able to quickly find out where you go and for how long.

Phone Updates- It is important to be aware of these updates because oftentimes they contain bug fixes and patches to problems in the older iterations of the software. Keep this in mind with your apps as well, if you let things get too far behind on updates, you risk data breaches and security threats.

Passwords- The most dangerous thing that people do with their smartphones is that they do not put a password on them. Fortunately, most software now requires you to put a password on your device. If you have a password on your phone, make sure it is a good one. In 2019 alone, “123456” was the most commonly used password, accounting for 23.2 million accounts. Your password is the gatekeeper to everything confidential in your life so don’t take this security step lightly. Tools like 1Password will help you manage and automatically generate lengthy passwords that are then stored in a vault that is protected by a PBKDF2-guarded master password that you create. Don’t sacrifice security for convenience.

Erase Data- This feature on your phone sounds scary, but hear us out. When you enable this feature, the first thing it does is turn on “data protection.” This is a powerful security mechanism and when it is enabled, it ensures that any files created by an app are automatically encrypted on your phone’s file system. This means that if someone were to come into the possession of your phone and you have a passcode on it, they would not be able to access any data stored on your device, even if they plug it into a computer.

Cloud Backups- Cloud backup enables your organization to send a copy of your cloud data to another location so that if your data is compromised, you can restore the information, ensure business continuity, and defend against devastating IT crises.

The Takeaway

All of these best practices serve to help you protect the information stored on your personal computer (your cellphone). It is important to note that “reasonable efforts” and “reasonable precautions” means reasonableness. Not perfection. You have an obligation to do what you can, stay informed, and mitigate risks. You do not have to be a technology or smartphone expert to practice the above-mentioned best tips.

How are changes in today’s climate impacting your law firm profitability? Technology has changed our world significantly, and law firms are slowly catching up to the rest of the business world in many areas. Gone are the days of the large offices, where every attorney has their own secretary, and the firm houses a large library full of books that must be manually updated with those supplements that would arrive on a regular basis, much to our chagrin.

As we have slowly joined the rest of the world in the ways of online research and paperless offices, we are also considering more appropriate ways to look at profitability. This is due, in part, to client demand. Clients no longer accept the idea that they will pay our firms by billable hour, with no budget or foreshadowing of what their final out-of-pocket expense may become. Technology allows for broader communication and stiffer competition, and if we want to remain competitive, we must become more efficient and readily able to consider alternative fee arrangements (AFAs) such as flat fees, risk collar agreements, etc., or at the very least, offer accurate budgets that clients can count on so that they know their worst-case scenario.

While we may have given in to the fact that we must agree to these terms in order to get the work, many firms find themselves no longer profitable as a result. Where they are falling short is in the failure to recognize that, like other businesses, they must have a cost accounting model that allows them to understand what their cost is for producing the client’s product before they can agree to a sale price.

If you think only manufacturing companies can use cost accounting methods in their businesses, think again. Law firms who are using these methodologies will leave behind those who don’t educate themselves in these practices. You may not be producing widgets, but you are selling a “product” (time) that can be measured in order to determine the cost to produce that product. By implementing a cost accounting system, you will be able to determine profitability by producer, department, office, client, and matter. (You may be surprised to learn that your largest fee income client is not necessarily the largest contributor to your bottom line!)

Determining the Cost of Your Product

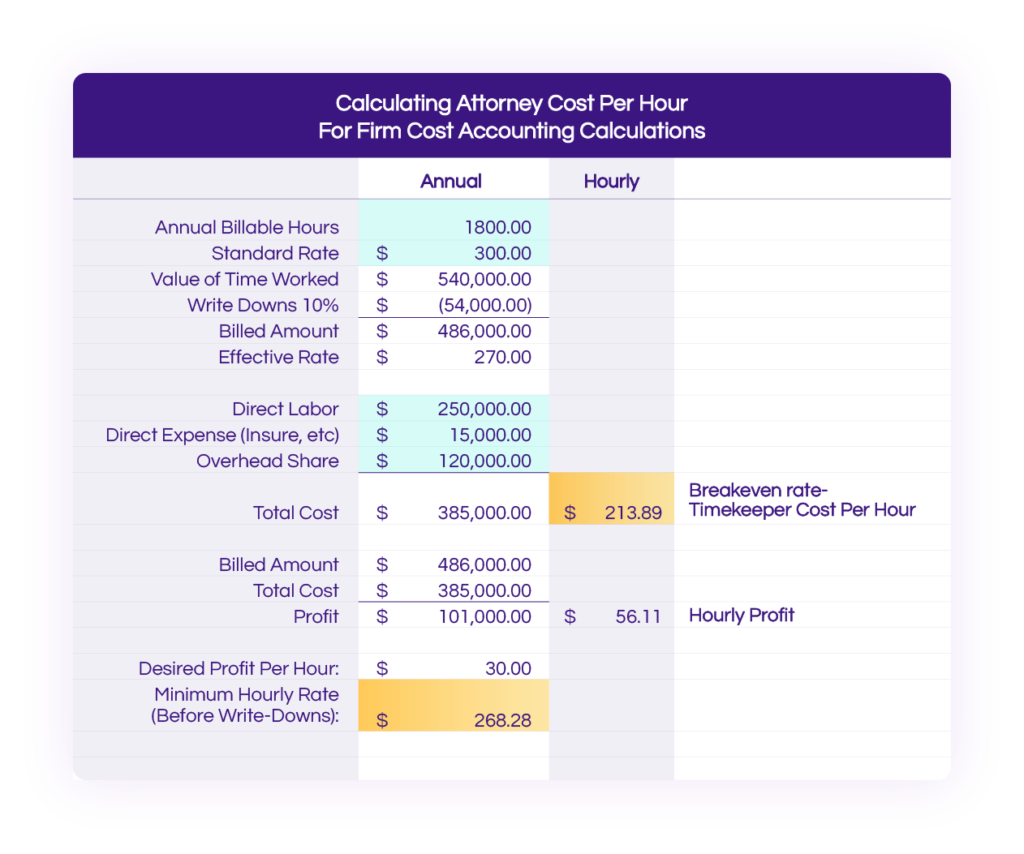

So how does a firm determine the cost of their product? It isn’t as complicated as you may think. By determining the direct costs of your timekeepers (salary, payroll taxes, insurance, training, etc.) and allocating the remaining firm overhead to your timekeepers (how the overhead is allocated to differing timekeepers is another article in itself), you can determine an annual cost per timekeeper. By then looking at the number of hours each timekeeper bills per year, you can determine their hourly cost. (Timekeeper annual cost including overhead allocation ÷ number of hours billed = timekeeper cost per hour.)

Once you have determined the timekeeper’s cost per hour, you can readily understand what you can (and cannot) afford to offer as your billable rates and AFAs. You can determine the necessary billable rate for each timekeeper in order to meet your profitability goals, taking into account anticipated write-downs and write-offs (typically 10 percent). You will also know very quickly whether you can afford to offer a client a discount on any given invoice and still receive a profit on that work.

See the example below:

The attorney bills 1800 hours per year at $300 per hour, for a value of $540k.

The sample firm typically sees 10% in write-downs and write-offs, placing the true value of the work at $486k.

This puts the attorney’s effective rate at $270 per hour.

The attorney’s total cost, including their share of the firm overhead, is $385k. At 1800 billable hours per year, this puts their break even rate at $213.89.

What does this spreadsheet tell you?

You need to receive a minimum of $213.89 for each of the attorney’s 1800 billable hours just to break even on this attorney.

At the current hours, rate, and costs, this attorney earns you $56.11 per hour.

If you have a goal of a profit of $30 per hour, the attorney needs to bill a minimum of $268.28 per hour to cover write-downs and write-offs, attorney costs, and get to the desired goal of $30 per hour profit.

How does that help you?

When considering client requests for discounts on their invoices, you know whether you can afford to agree to the client request without losing money.

When considering AFAs, if you know how many hours a project should take you, you can easily come to a flat fee that will meet your desired profitability goals.

When considering whether a client is truly profitable, you know what your baseline number is. Many times our biggest clients expect deep discounts because they “pay us a lot of money.” With this information you can break it down – by looking at who your timekeepers were for an individual client, how much they billed and what their bottom line hourly rate is, you know whether the client is truly profitable to the firm, or whether they are costing you money despite the total amount they spend in fees each year.

By doing a small amount of legwork on the front end to create a model that works for your firm, you can

Ensure you are billing your timekeepers at a rate that will meet your profitability goals;

Look at the profitability of each client based on the timekeepers who have worked on their matter(s) and the effective rates for those timekeepers after receipts;

Be more accurate in your budgeting for client proposals;

Be more competitive by using this knowledge to be creative in your billing models and the use of AFAs.

One final note – be sure to require your attorneys to capture their hours, even on flat fees and other AFA arrangements. If you don’t, you will not be able to determine how successful your AFA models are working for you in helping you to maintain profitability.

There are a lot of fancy definitions for the term “strategic planning.” But at its core, all it means is to pinpoint a direction you want to go and then make decisions on how you plan on allocating your resources to get there. It is important to see the difference between strategic planning and marketing. And you may raise an eyebrow at that, but you’d be surprised how often people view these as the same thing. Strategic planning encompasses many operations of your business. Marketing is merely a piece of that coupled with things like your budgeting and reporting.

It is very important to note that strategic planning is not about grand ideas or mission statements. It is about where you want to be and how you’re going to get there, all within a short and defined timeframe that is typically no longer than 5 years at a time.

Typically, smaller firms can respond more quickly to changing conditions than larger firms, and because of this, there is a temptation for the smaller firms to get lackadaisical in their planning. Larger firms know that it is significantly harder to pivot, so they prepare and they do not take their strategic planning lightly.

Key Elements to Strategic Planning

Top-down planning process

From a high level, strategic planning consists of what we call a top-down planning process. Your firm has to first set the overall goal and then create a realistic framework and path that will allow you to get there.

Measurable objectives

For instance, if you set a goal for your firm to have a family law practice area in two years, the next question you have to immediately start asking is how are you going to achieve that? Your goals must always be measurable. Period. There have to be measurable objectives, otherwise reaching that end target is going to be very difficult and you’ll be more likely to set goals that are unrealistic in that proposed time period.

Resource analysis

Once you’ve set your goal and defined your measurable objectives, the next thing you need to do is analyze your resources. What skills do you already have within your law practice and if you’re missing skills, what are you going to do to fill those gaps? Are you going to go out and learn them or are you going to hire people with those skills? When you begin analyzing your results, you need to also ask yourself, what do you need to get there? Sometimes firms will opt to hire an outside consultant to help guide them, others prefer to make those decisions on their own. Either way, you should figure out what assets you have and which assets you still need.

Regular status meetings

Schedules are busy, but it is essential that you and your team find time to pencil in status meetings into your calendar. Part of the reason you set measurable goals is so that you can measure them. These meetings don’t have to be once a week, they could be bi-weekly or once a month, but they do need to happen, and you do need to communicate with your team and constantly be monitoring your progress. Time always moves faster than you think, don’t let timelines and due dates sneak up on you.

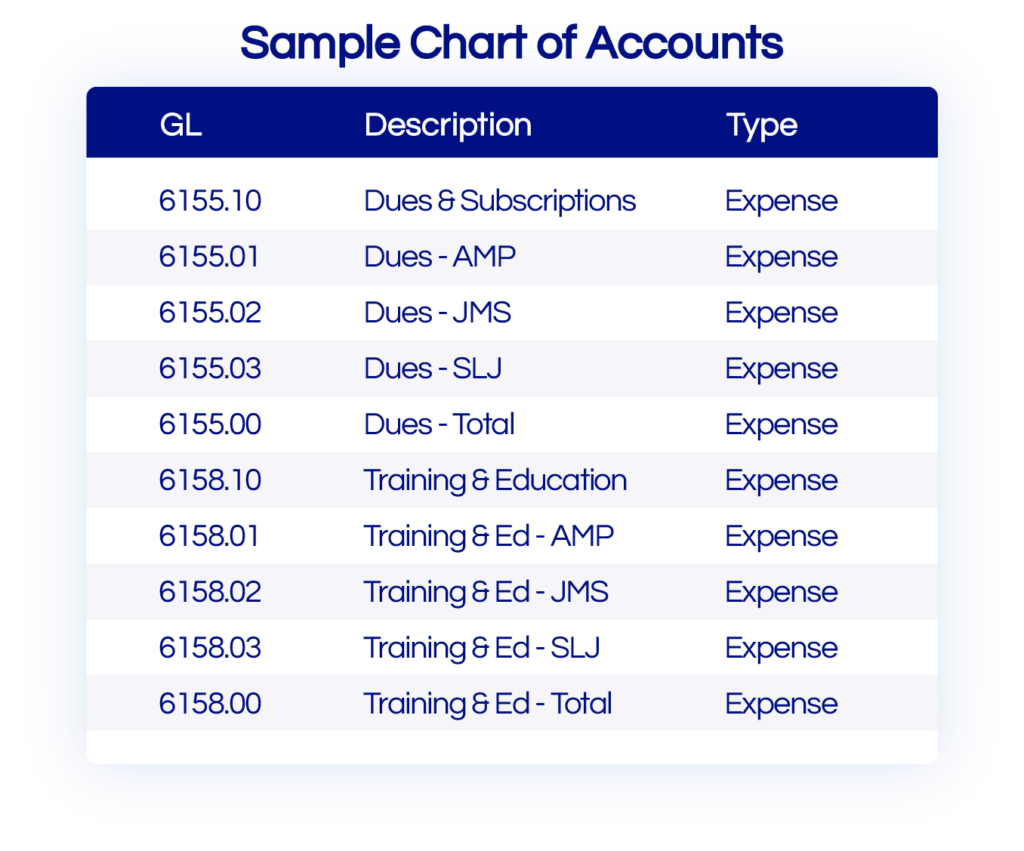

Budget

Set a reasonable budget and adhere to it. You need to be asking yourself, what does your law firm's cash flow look like this year? How about your net income by year-end? Having a quality budget in place removes the guesswork and ensures you end up where you want to go. Additionally, ensure you have a good general ledger chart of accounts. If you are not familiar with the chart of accounts, it is simply a list of income and expense categories used to track your spending. Building a budget is a very crucial step in the process, if you’re wavering on how to begin, check out our 4 tips on building a better budget.

How to Plan

Planning is not everyone’s strong suit and that’s okay! However, having the ability to plan is crucial when you begin targeting and mapping out your firm’s future. Fortunately, being a planner is a learned skill for most people. But they say you don’t know what you don’t know, so if you’re unsure if you fall into this category, there are plenty of personality tests that you can take that will give you an idea of what your strengths and weaknesses are. The Myers-Briggs Type Indicator® is a great resource if you’re curious! Additionally, check out seminars from the American Management Association and the Chamber of Commerce.

Financial Basics

Strategic planning sounds great, right? But what if you don’t have the financial background to adequately develop these plans? Don’t sweat it, you don’t need to have a degree in economics to know what you’re doing.

The key is to have a benchmark or expectation to see why your actual figures differ from expectations and take action based on what you find. The expectation in our financial management function is why we need a strategic plan and a sound budget. To start, use current and past budgets to create an expectation. Don’t make this part harder than it needs to be, take the information you already have and use it to build out the broader picture.

There are five basic financial statements you should be reviewing every month to help your strategic planning efforts:

Balance Sheet

Income Statement

Statement of Cash Flow

Owners’ Equity Statement

Budget

The Balance Sheet

This shows the financial position of a company at a specific point in time. This is usually run or prepared the first week after the close of each month. So if you’re going to look at your March financials, for example, you’re going to run them the first week of April.

This is why it is so critical that you have all of the financial transactions posted to your chart of accounts on a timely basis. If you’re at a larger firm and the accounting team starts putting pressure on you to get your timesheets in, this is why. If you haven’t posted all your costs, advances, your time, and complete your billing, then your reports will not be accurate.

Remember this formula: Assets = Liabilities + Equity

Your balance sheet is somewhat customizable when you’re comparing your designated points in time. You could choose to report on your current month, your activity year-to-date in a comparison against budget, or it could show you year-to-date in previous years. If you’re using a practice management system, you should have the ability to generate such reports. It is important to note that not every software gives you the ability to customize your reports whenever you want them. Many vendors will only offer boxed, off-the-shelf reports, so be wary of this, as typically firms end up needing more flexibility in their reporting than they initially expect or anticipate.

Income Statement

This reports on a company’s revenue and expenses over a period of time. Typically, the income statement is reported every month. Most law firms tend to lean towards cash basis accounting meaning that revenue is not earned until it has been received. Therefore, your income statement and balance sheet do not show accounts receivable or WIP. Those are separate, internal reports that you can run with your accounting software. Keep in mind that although these reports are run separately, they are crucial for your law practice.

We cannot express to you enough how essential it is to have a good chart of accounts so that your reports are meaningful. An issue that will make your accounting reports difficult to read is if there is not enough account detail in those chart of accounts. The chart of accounts should reflect the way your law firm is organized, for example (to name just a few) you could have reproduction expense, marketing expense, technology expense, partner compensation expense, etc. Doing this will make your reports more specific and meaningful to you.

Now, when you’re looking at gross profit and net income, or net profit, an important test to conduct is to look at your top paying clients and add up what these people or groups are earning for your firm. Then take that number and look at it as a percentage of the gross revenue. This is a good indication of how flexible your law practice would be if you suddenly lost that work. An even more telling test would be to do that same calculation, take your most lucrative type of work, and view that as a percentage of your net income. For a lot of law practices, this can be quite scary because it will show that they have very little to no flexibility at all.

Statement of Cash Flow

This reconciles net income to the change in cash by showing sources and uses of the cash.

On cash flow statements, you’ll typically see net income first, followed by adjustments in reconciled net income, cash from operating activities, and depreciation. Other line items you might have include cash flows from investing activities and financing activities.

Owner’s Equity Statement

The owners’ equity statement outlines the changes in the owners’ equity accounts during the year.

In this statement, you will have members’ equity at the beginning of the year, then any contributions added by those members, added net income (money before distributions), and then finally the members’ equity at the end of the year following the dispersal of those distributions.

Putting it all Together

Now that we have taken a high-level look at these key statements, how do they all relate to each other? Are they even connected? Do they make a difference when you begin thinking about your strategic plan for the future of your firm? Let’s see...

So let’s look at the balance sheet, statement of owner's equity, the cash flow statement, and the income statement. If you look at your cash, this will be showing on your balance sheet and your cash flow statement. Your net income is also shown on your statement of owners’ equity, the cash flow statement, and it is also shown on the income statement. Owners’ equity is shown on the balance sheet, and of course on the statement of owners’ equity as well.

So you can see why naturally, all the statements have to balance and agree with each other. They are all interconnected and work to provide checks and balances to your firm.

All of these statements will ensure that your books are balanced and in order. Without this information, you will not be able to strategically plan for your future. Finance is all about the details and monitoring the cash coming in and the cash coming out of your firm. You don’t have to go at this alone, technology today has made it much easier to strategically plan and build out these reports the way you need them. If you’re unsure of where to start, take a breath, think about the direction your firm wants to go, and slowly begin mapping out how you will get there.

What does your law firm's cash flow look like this year? How about your net income by year-end? Having a quality budget in place removes the guesswork and fear from your financial picture and ensures you end up where you want to go. We have all heard the phrase, “Failing to plan means planning to fail.” A good budget will not only help to forecast net income and cash flow, but it will help you to plan for potential problems before they become emergencies.

The two most common types of budgets are zero-based and incremental. If you are a new firm with little to no history, you will need to start with a zero-based budget. A zero-based budget is just what it sounds like – you start at zero and forecast each expense you anticipate incurring, as well as the revenue you hope to achieve.

With incremental budgeting, you have the luxury of looking back at your history and creating the next year’s budget based on what you have experienced before. Be careful though – with incremental budgeting, it can be easy to fall back on past numbers with little effort made to improve efficiencies and drill down on ways you can do better.

Regardless of the approach you take, the first step is to ensure you have a good general ledger chart of accounts. If you are not familiar with the chart of accounts, it is simply a list of income and expense categories used to track your spending. In a law firm, typically your income is fee income. You may also have a rental income if you own a building and rent a portion of it to other tenants. When it comes to expenses, you want to find the happy medium between having enough detail to aid you in future years without having so much detail that it is a cumbersome system to use. It is also helpful to ensure you keep any expenses pertaining to meals separate – your CPA will need to know that number at tax time because your meals are not 100% deductible!

Steps to Creating Your Budget

Step 1: Plan

Don’t plan in a vacuum. Start by reaching out to all stakeholders in your firm. What do their CLE expenses look like for the year? Any conferences planned? How is the equipment looking? Is anyone going to need any major purchases to replace outdated equipment? What about staffing? If leadership is planning to add more employees to the firm, you need to know whether you are going to have the money to cash flow that addition. Attorneys typically take six months before they show a profit for the firm.

Step 2: Insert Your Plan Into a Spreadsheet

It is helpful to use a spreadsheet for planning your budget. You should have a sheet for income, a sheet for expenses, and a sheet that links the bottom line of your total income and expenses so that you can see your forecast net income.

Begin your budget by estimating income. In your budget spreadsheet, you can estimate the fee income for each timekeeper in your firm. It is a simple list for each timekeeper, with their estimated billable hours for the year multiplied by their average realization rate. Your financial software may be able to run this realization report for you – if it does not, you can estimate a fairly accurate number by looking at the timekeeper’s previous history and dividing their fee receipts by their billable hours. If your firm has any contingency matters, don’t forget to account for them as well – some may be at a stage where there is guaranteed income to the firm, and some may still be truly contingencies – you should account for the contingencies in a separate line item that is not counted on.

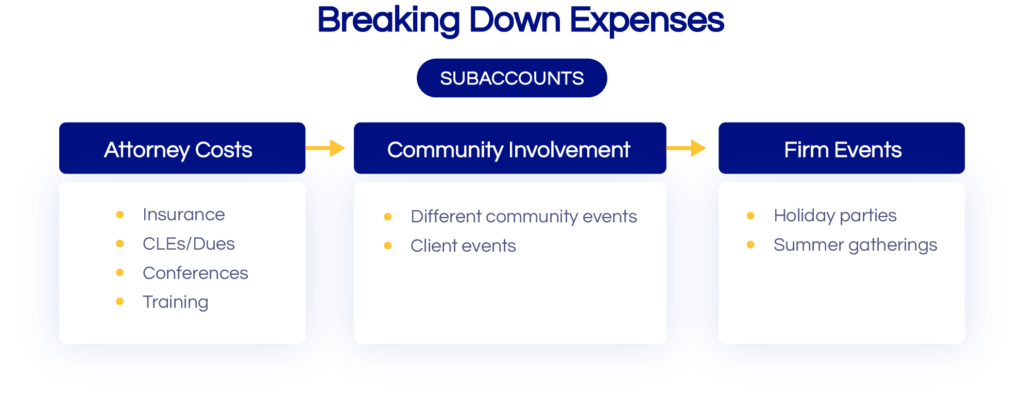

When it comes to budgeting for your expenses, be sure you have a good plan for your GL accounts before you start. Try to anticipate everything you may want to be able to track in the future. Your financial software should allow you to have parent accounts and sub-accounts. For example, you may have a set budget for firm events for the year, but you may want to be able to track what the firm spends on the annual holiday party v. its summer outing and its annual Administrative Professionals’ Day celebration. You can have a parent account for firm events, with sub-accounts for each of those sub-items. This will allow you to easily plan in future years by having a quick picture of your historical spending.

Another great way to use sub-accounts is to track costs the firm incurs for each attorney. Examples include insurance, association dues, CLEs, conferences attended, etc. By creating a sub-account for each attorney, it is very easy to run a report from your financial system to track their direct costs when you want to determine their true profitability for the firm.

Step 3: Look at Your Bottom Line

When you have completed your income and expense entries into your spreadsheet, ensure that you end up with the desired net income at the end. If you don’t, you need to sharpen your pencil!

Step 4: Enter Your Budget Into Your Financial System

When it comes to entering your budget into your financial system, be sure you are entering the expenses in the month that you expect them to occur. Some items will be spread equally throughout the year, like rent and equipment leases. Others will occur in specific months, like professional liability renewals and holiday parties. By planning for your professional liability renewal to occur in the appropriate month, you can have your eye on the ball in cash flow planning and avoid the extra expense of paying for financing your premium.

Don’t Just “Set It and Forget It”

Use your budget for decision-making. If someone is requesting something that was not planned in the budget, is it necessary? Is it something that can wait until next year? If not, is there a way you can make up for the added expense by changing your spending in some other areas or increasing firm revenue?

Once you have entered your budget into your system, make sure you monitor it regularly. You should be running a monthly YTD income v. budget report to track how you are doing against your budget. Don’t despair if you see variances v. your budget. No budget is perfect, but by having one in place and monitoring it regularly, you can prevent any big surprises and make contingency planning when necessary.

What does it mean to have an international deposition? This simply means that the witness will be in a foreign country. However, in this new virtual reality we're in, there are new challenges and components that we didn't have to deal with before. Between juggling the complexities of international depositions, paired with the logistical and tactical struggles of video conferencing, you will have a lot on your plate.

As you begin navigating this process, there are some basic steps you should be taking that will hopefully make your depositions run as smoothly as possible. Let's check them out.

Steps to Conduct an International Deposition

Step 1

Leading up to an international deposition, it is recommended that 4-6 weeks prior to the deposition date, you determine whether the witness is even willing to be deposed and immediately begin coordinating with the opposing counsel.

Cooperative Opposing Counsel

If you have a good working relationship with the opposing counsel, the first thing you should be trying to check off your list is a mutual stipulation with the opposing counsel so that the depositions can move forward. You should be stipulating that:

The deposition will move forward remotely

The witness can be sworn in by a court reporter as long as both parties stipulate on the record and the court reporter agrees

This is extremely important because court reporters only operate in the country and or state where they are certified and registered, even domestically.

Uncooperative Opposing Counsel

What happens if opposing counsel is not cooperative? There are a number of options that we will touch on at a high-level:

The Consulate Office may have to administer the oath for the witness. This means that the US Consulate and whatever country the witness may be in has granted status to administer the oath as it was taking place on US soil.

The other option is to hire a local notary. This will always be contingent on the country’s laws and rules.

There are a few other judicial remedies where the judge by motion or otherwise decides to order that the deposition moves forward. This completely depends on the country where the witness will be.

Step 2

Now that you have talked to opposing counsel, hopefully, they are cooperative, the next step is to decide what country the deposition is going to take place in. There are a few red flags we want to draw your attention to with this.

The UK and Hong Kong are the most common locations for international depositions, but if you hear countries like Germany and Japan, those are extremely difficult to operate through and if you hear countries like Brazil or Russia, they do not allow US depositions to take place. A lot of the European countries that are in the EU are underneath the Hague Convention and generally follow the same rules. Please do your due diligence here because these rules do apply differently to citizens of those countries, versus non-citizens.

Remember that Covid considerations do apply to all depositions and meetings. Check out Our World in Data for up-to-date information on which countries are open, which countries will allow your team, opposing counsel, and or the court reporter to travel.

Step 3

Now that you have your country, you’ve spoken to opposing counsel regarding all the logistics surrounding the deposition, you must then determine where specifically the deposition will take place.

Much like a remote deposition here in the US, you have to decide the following:

Do you want the witness physcially with the court reporter?

Are you going to do this in a hotel, conference room, at the witnesses home?

Does it have to be at the Consulate Office for the purpose of swearing in the witness?

If the deposition must take place at the Consulate, it is recommended to start making those arrangements at least 6 weeks out.

With remote depositions, even domestically, regardless of where the witness will be during that deposition, you must test the equipment they will be using on the day of the deposition. And to go one step further, you need to make sure they have a working and reliable internet connection.

Whatever video conferencing platform you choose to use, your team needs to ensure that it has the capability to incorporate international phone numbers. This is important because if the internet connection is poor, and the bandwidth cannot sustain the meeting, the witness must have an option to call in and have video only.

Any video remote depositions do require a certain internet bandwidth speed, so again, please conduct your tech tests and be prepared.

Step 4

At this point, you’ve spoken to opposing counsel, you know the country, you’ve pinpointed an exact location of where your witness will be, you have all your equipment tested, next, you need to know what deposition services will be required.

To start, you need a court reporter, as mentioned previously, are you going to stipulate with opposing counsel that the court reporter be the one to swear in the witness remotely?

Will you have a videographer? Now, there is a common misperception with this element. Most online conferencing platforms have the ability to record meetings. But if that recording is taken on your own, it is not certified. Not to mention opposing counsel may not approve or allow it. So if you’d like the deposition recorded, you do need a certified videographer who can do the video recording remotely. This is a highly encouraged practice for international depositions and locally-based ones as well.

Do you need an interpreter? If so, what language(s) do they need to be able to speak, do they have all the necessary and properly tested equipment?

Next, you need to think about your exhibits. What exhibit platform are you going to use? Are you going to show your exhibits by sharing your screen? Some conferencing platforms will let you share you exhibits by chat, so is that something you would consider using? Additionally, how, when, and to who will you submit your exhibits to? Take time to get all these answers organized.

Following these considerations, the next step for your team is to prepare and send your deposition notice with all the assets and people you’re requesting for the deposition. It’s best practice to always indicate that this will be remote and by video conference. You also may want to take this opportunity to identify any other unique aspects of the deposition.

Step 5

It is important to send out your notice to the agency you are going to use to arrange your court reporter, as soon as possible. If there is an issue in terms of stipulations, you may need, for example, a notary in that country and that process takes time to coordinate. Any logistics internationally presume will take at least a week longer than in the states.

Step 6

It’s deposition time! Make sure you have the time correctly marked in your calendar, and everyone is on the same page in terms of time zones.

When it begins, it will flow like a normal domestic deposition, just keep in mind any other additional considerations or international rules that you have to follow.

The Takeaway

Whether you’re working with an agency that specializes in international depositions or not, be prepared and do your homework. Make sure you leave yourself plenty of time to schedule and coordinate everything so that you have time to make adjustments if need be.

Today’s reality looks something like this: we wake up slightly later because the longest commute we now face is walking from our bathrooms to the kitchen. Dogs barking in the background, kids running in the background, and a home office set-up that would make Office Depot proud.

Working from home is our reality and although we have quickly adapted to this change, some industries face hurdles that far outweigh others.

Unfortunately, the legal industry is not exempt from the hardships that work from home has caused. Sure we have telephones and Slack and other means of communication, but by removing the element of face-to-face interactions, we have also removed a certain element of humanity. Your clients are stressed more often than not and now that we are forced apart, how do we bridge that connectivity gap? How do we create an environment of togetherness and empathy even if we are miles away from each other?

This dilemma carries into the courtroom as well. And arguably, it is harder to get away with the virtual nature of the work you conduct because a courtroom relies on this element of connectivity. But if you exchange your courtroom nuances with that of a screen, what do you get? Will the results be the same as they would if you were there in person? The goal is for that answer to be yes. And we are here to help.

So let’s talk about one dilemma that many attorneys face and that is “how do we manage exhibits in a virtual courtroom?”

Going to court looks different and because of this, the processes and procedures we may have followed at one point now have changed.

In this virtual world, there are some steps you should follow when moving an exhibit in. Take a look:

1. Know Your Court’s Requirements

Each court and each judge has different requirements when it comes to how, when, and to whom you need to submit your exhibits.

Most still require you to submit your exhibits to the clerk, but you can guarantee that they will be required to be sent in a virtual format by a specific deadline prior to your hearing or trial.

Some require a courtesy copy of those exhibits to be sent to the judge through the JA. So you want to make sure you know and understand where the exhibits need to go and in what format they need to be in. Do they need to be in a PDF format, do photos need to be JPEGs? You have to make sure you are understanding the requirements.

Some require the exhibits to be submitted through an online portal. Ultimately, you want to make sure that the first thing you know and understand is “how,” to submit exhibits, what format those exhibits are expected to be submitted in, and to whom those exhibits need to be submitted to.

This should go without saying, but do not miss your deadline. If this happens, that could result in a delay of your hearing or trial.

Once you have this covered, guess what? The rest of it is almost the same!

2. Moving an Exhibit In

If you know how to move an exhibit in court, you know how to move an exhibit in on Zoom. That doesn’t change. The medium does not change the process for moving in an exhibit. Your exhibit still has to be relevant, related, and right.

Your exhibit needs to be relevant, meaning it proves or disproves a fact of consequence.

They have to be reliable, meaning they are either not hearsay, or there is an applicable hearsay exception.

And they have to be right, meaning as in not prejudicial.

Once those three things exist, you’re going to go through the same “do,” “how,” “what” process.

Do you recognize it? How do you recognize it? What is it?

And then the remainder of the predicate depends on what type of exhibit you are moving in. However, in this virtual world, there are some things you do have to do differently.

3. Verbal Communication Differences

You no longer have to say “I’m showing opposing council, what has been pre-marked as defense exhibit A for identification purposes.” Why? Because you’re not actually making that movement in the courtroom where you’d need the court reporter to document it.

What you do need to say is “I’m putting up on the screen, what has been pre-marked as defense Exhibit A for identification purposes,” so that your court reporter still can take down the exhibit and make sure that it is a part of your record.

When you are doing the logistics of moving the exhibit in, you also do not have to ask to approach the witness. This sounds fundamental, but you will be surprised. Because you have been doing it for so long in a certain manner over and over again, the first time you have to do it in this virtual setting can feel very weird. You’re going to want to say, “I’m showing opposing council, what has been pre-marked as defense Exhibit A for identification purposes. Your Honor, may I approach the witness?” You don’t have to do any of that. But you do still want to make it clear for your record, what you’re doing and what exhibit you're handling. You can ask the witness to go to what’s been marked as Exhibit A, and they can now pull it up in whatever format it is that they have it in.

4. Formatting

When it comes to formatting for your witness, your judge, or even the opposing council, we suggest using a PDF document that you can bookmark. And you bookmark it in the order you want to proceed in. In an ideal world, your exhibit list matches the order you intend to introduce your exhibits in trial.

No one lives in that type of ideal world. It almost always gets reordered once you do your trial notebook, and you start doing your questions.

So what you want to do is make sure your final PDF is bookmarked in the order you want to introduce the exhibits in. Doing this will make it easier for your client who is going to be your witness. It also makes it easier for the judge to follow because when it is a bookmarked PDF, the judge can just click on the bookmark and it automatically takes them to that exhibit. It is also recommended to put the exhibit letter, or a virtual exhibit sticker on the appropriate PDF pages themselves to keep them organized. Some ways you can do this include inserting a footer or by using the bate stamps feature that is in PDF.

Your organization is what becomes key in this virtual setting. And as we mentioned before, moving the exhibit in and the trial skills associated have not changed, the process has. Your clerk, your witnesses, and the judge all need to know what you’re talking about, so this organization is paramount.

5. Using the Exhibit

When you are getting ready to use the exhibit, you’re going to have to share your screen. Prior to doing so, you have to ask the judge’s permission to do that. In some cases, the judge will explicitly say that the council has permission to share their screen when necessary.

When getting ready to share your screen, your exhibits should still satisfy the “Billboard Test.” There are a number of ways to be able to use exhibits and do presentations in this virtual setting. Powerpoint is going to be the most common default presentation application for most attorneys. If you choose to operate from PowerPoint, you do not want a million words on each slide. You want to satisfy the Billboard Test. What is the Billboard Test you may ask? When you’re driving down the street and you see a billboard, it has all the information you need, in large print with no clutter. You can understand who the billboard is about, what the contact information is and you’re able to digest that information in the 2.5 seconds you have to look at that billboard.

You want to apply this same test to your exhibits and your presentations. If you’re using your PowerPoint for your opening, or closing statements, or any other kind of demonstrative situation, make sure it is clear. Make sure they can read it, and don’t put any overwhelming amount of information on it. Er on the side of having more slides with fewer words than condensing the quantity and packing everything you have to say on three slides. If the people on the other side of the presentation cannot quickly read or understand what is on the screen, you’re going to lose them.

Because we are in a virtual environment, you must be able to convey the information that you need to convey in a clear and concise manner. When dealing with an actual exhibit, and in this hypothetical case let’s go with medical records. When you are using these documents, unless you need the entire document, it is suggested to do a call-out. This call-out would work similarly to the way you normally would do a call-out if you were standing at trial in person.

Using this call-out draws the attention to wherever it is you need it to be. You still have to use the entire document in order to get it authenticated and introduced, but when you get ready to actually use the actual exhibit, use the pertinent parts! This will work to cut down clutter, and the person not being able to see or understand where it is you’re coming from.

6. Tangible Exhibits

When it comes to physical and tangible exhibits, you need to submit all physical items to the clerk in order to get it entered. Have a photograph of it, so you can use it and talk about it and everyone can see what you’re talking about. If for whatever reason, the court lets you keep this physical exhibit (they really shouldn’t because if you’re entering this piece as evidence, it needs to go into the court’s virtual file), you should still have photos taken of the item to share electronically throughout the Zoom presentation.

Takeaways

Although our world has changed slightly, life still moves forward, even if not in a way we imagined.

When it comes to your exhibits, make sure they are clearly marked and organized and are being presented in a clear and concise manner. Remember, you should be handling them the same way you would handle them in physical court, you’re merely adjusting how you submit and introduce them.

In, Accounting 101 for Law Firms we discussed how when firms are asked, “How do you want to define growth?” The leading response is always through revenue.

That is great, right?! “Revenue.” We all love this word, it’s great a great way to track performance, but how do you actually track revenue? Is it as easy as simply counting the dollars that come through your door? We wish.

The first thing you need to do is start utilizing KPIs. Your key performance indicators will be your best friends and the figures you need in order to answer the question, “how do I track my firm’s revenue?” It is important to note that these indicators are merely that, indicators. You should use them as a guide and lean on customized reports to really gain valuable insight into the productivity and performance of your firm.

At the end of the day, your firm is a business, so although you have spent 10,000+ hours honing your craft as an attorney or legal professional, you still have to be able to wear that business hat to keep the lights on.

That may sound dreadful, but don’t let the idea of numbers discourage you! These metrics can be used to help you make real-time business decisions that are going to greatly impact the future of your firm.

Profit Margin

To jump right in, let’s talk about profit margins. That is how many cents on the dollar are you able to push into your pocket at the end of the day. If it is 35%, that means you get $0.35 of every dollar at the end of the day. Your profit margin can be looked at as your net income divided by your revenue.

[cb_calculator name="Profit Margin" title=" "]

Average Rate Billed Per Hour

Next, think about how much your time is actually worth, or rather, your average rate billed per hour. This can be calculated over multiple time frames, but make sure the time frames you choose are always the same. So if you’re looking at the total hours billed for the month, don’t divide it by the total hours billed for the quarter. All of your time frames must match, otherwise, you’re comparing apples to oranges. You can calculate this amount by dividing the total hours billed for whatever time period you’re looking at, by the total dollars billed in that same period.

[cb_calculator name="AVG Rate Billed Per Hour" title=" " formula="Average Rate Billed Per Hour = Total Dollars Billed / Total Hours Billed"]

Collection Percentage

The next KPI is important: your collection percentage. You work hard week in and week out, and although you may know how many hours you billed each week, do you know how many of those hours you’re actually getting paid on? It is easy to rattle off those initial billable numbers, but the numbers you have to dig for below the surface are much more valuable. So when you’re thinking about your collection percentage, take the total cash you have collected in a time period and divide it by the total dollar amount billed in that time period.

[cb_calculator name="Collection %" title=" "]

Operating Expense Per Timekeeper

Some more advanced ratios include things like how much do you spend per timekeeper at your firm? This is very important to look at. All you need to do here is take your total operating expense that you would get from your Profit and Loss statement and divide it by the number of timekeepers at your firm. This is going to give you a really great insight into how much it costs to actually run your business.

[cb_calculator name="Operating Expense Per Timekeeper" title=" "]

Profitability by Client

Where it gets interesting is where you can use the figure you calculated from the operating expense per timekeeper to determine if you and your team are working on profitable clients. Profitability by client is huge because as you start to unpack this, you can quickly determine which of your clients truly brings your firm more revenue and which are just eating up your time. Everyone has a few clients where it costs you more to serve them, even though you may have higher billing rates. The problem with this is that most firms do not pinpoint these clients until the work is already done. So, to determine your profitability by client, simply take the fees generated by the client and subtract that estimated cost per timekeeper per hour worked.

[cb_calculator name="Profitability by Client" title=" "]

Utilization Rate

Lastly, are you hitting your targets? Your firm’s utilization is important because the more informed you can be about your productivity, the easier it will be to make decisions on matters like staff expansion. Is an extra timekeeper necessary for your growth or can you manage by simply shifting staff around? How do you determine what the right thing to do is? To calculate this utilization percentage, divide the total billable hours of a timekeeper by their total working hours. This percent may fluctuate throughout the year based on caseload, so it is important to keep your external factors in mind when making considerations for your staff.

[cb_calculator name="Utilization" title=" "]

There are many KPIs and reports you can generate and use to monitor and track your firm’s revenue. You don’t have to be a finance buff or accounting expert to do this math, and once you start incorporating it into your weekly or monthly routine, it will become second nature! Until that time, we have tried to make it as easy as possible for you to get a handle on your numbers, so we have created a KPI calculator that you can access here to get you started!

Everyone handles their email inbox differently. Some people have to clear every unread message out at the end of each day, while others let their unread email notifications pile up until there’s no going back. But one thing is for certain, our inboxes today are significantly more overwhelming than they were even just a few years ago.

Before we jump into email management and everything therein, we are going to take a moment to talk about a psychological philosophy called Flow. Essentially, Flow is a state of mind in which a person becomes fully immersed in an activity. While this is a mental state, it is deeply influenced by psychological, environmental, creative, and social responses.

Your chances of reaching this Flow state are greater when you can first focus on single tasks, as opposed to jumping back and forth between activities. Additionally, having clear goals and immediate feedback play into your ability to reach Flow.

Now you may be asking why we are bringing this up now when we’re supposed to be talking about emails. And we will tell you… Emails are huge disrupters to our Flow state because each email we receive acts as a distraction from our current task. Not only are we interrupted to either respond or read the email, but we are given yet one more thing to focus on. Emails are inevitable. They are a great means to communicate, but if unmanaged, they can quickly spin out of control.

Now that you have a brief background on Flow, everything we discuss moving forward is to help you achieve this level of clarity and productivity through your inbox.

To kick this off, let’s look at some numbers. Did you know that the average office worker receives around 121 emails every workday? Roughly 2.5 hours a day are spent on email, which adds up to about 30% of your workweek! That is insane… Nowhere in your job description does it say you have to spend 30% of your time on email, but this is where we are today.

Three things are significantly impacted by our time spent on email: our mood, our focus, and our to-do list. These three things are both negatively and positively impacted by not only the quantity of virtual mail we receive in a day but the quality as well.

The Science Behind Attention

For the past few decades, a lot of studies and work have gone into the science of attention. And because our inbox holds so much of our attention during the day, there are many parallels that can be drawn between our inbox and our phycological response to how we interact with that inbox. Part of why so much our of time is devoted to checking and looking at our email can be attributed to what science calls the Fixed reward vs. the Variable reward system.

Hear us out, this is interesting…

In 1948, a behavioral psychologist B. F. Skinner studied what he coined “schedules of reinforcement.” At the time, what Skinner was studying was the relationship between actions (in his case, a hungry rat pressing a lever in a so-called Skinner box) and their associated rewards (pellets of food). During this study, Skinner distinguished between fixed-ratio schedules of reinforcement and variable-ratio schedules of reinforcement. Under a fixed schedule, a rat received a reward of food after it pressed the lever a fixed number of times — say 20 times. Under the variable schedule, the rat earned the food pellet after it pressed the lever a random number of times. So for example, if the rat pressed the level 5 times he would get a reward, and sometimes it would take pressing the lever 150 times to get the reward.

Obviously, the predominant difference between the two schedules of reinforcement was this aspect of predictability. Prior to the conclusion of the study, one might expect that the fixed schedules of reinforcement would be more motivating and rewarding because the rat can learn to predict the outcome of his work. Instead, what Skinner found was that the variable schedules were actually more motivating. The most telling result was that when the rewards ceased, the rats that were under the fixed schedules stopped working almost immediately, but those under the variable schedules kept working for a considerable time longer.