Get a Free Demo

What does your law firm's cash flow look like this year? How about your net income by year-end? Having a quality budget in place removes the guesswork and fear from your financial picture and ensures you end up where you want to go. We have all heard the phrase, “Failing to plan means planning to fail.” A good budget will not only help to forecast net income and cash flow, but it will help you to plan for potential problems before they become emergencies.

The two most common types of budgets are zero-based and incremental. If you are a new firm with little to no history, you will need to start with a zero-based budget. A zero-based budget is just what it sounds like – you start at zero and forecast each expense you anticipate incurring, as well as the revenue you hope to achieve.

With incremental budgeting, you have the luxury of looking back at your history and creating the next year’s budget based on what you have experienced before. Be careful though – with incremental budgeting, it can be easy to fall back on past numbers with little effort made to improve efficiencies and drill down on ways you can do better.

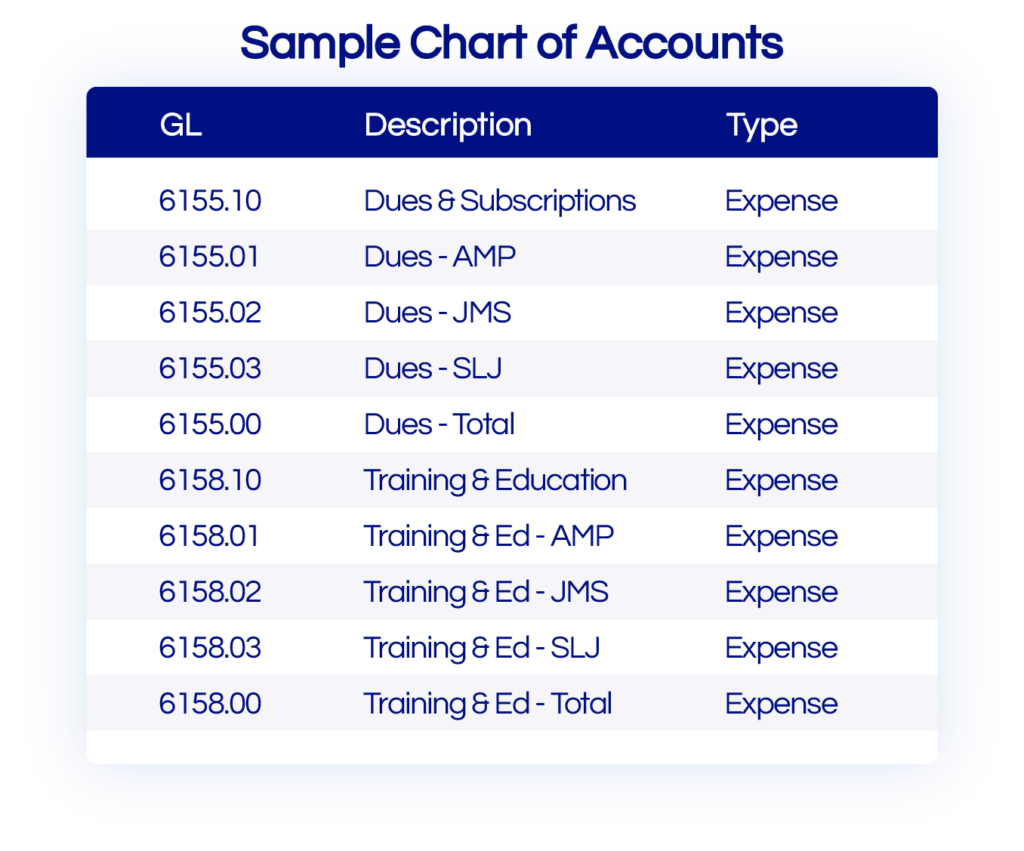

Regardless of the approach you take, the first step is to ensure you have a good general ledger chart of accounts. If you are not familiar with the chart of accounts, it is simply a list of income and expense categories used to track your spending. In a law firm, typically your income is fee income. You may also have a rental income if you own a building and rent a portion of it to other tenants. When it comes to expenses, you want to find the happy medium between having enough detail to aid you in future years without having so much detail that it is a cumbersome system to use. It is also helpful to ensure you keep any expenses pertaining to meals separate – your CPA will need to know that number at tax time because your meals are not 100% deductible!

Don’t plan in a vacuum. Start by reaching out to all stakeholders in your firm. What do their CLE expenses look like for the year? Any conferences planned? How is the equipment looking? Is anyone going to need any major purchases to replace outdated equipment? What about staffing? If leadership is planning to add more employees to the firm, you need to know whether you are going to have the money to cash flow that addition. Attorneys typically take six months before they show a profit for the firm.

It is helpful to use a spreadsheet for planning your budget. You should have a sheet for income, a sheet for expenses, and a sheet that links the bottom line of your total income and expenses so that you can see your forecast net income.

Begin your budget by estimating income. In your budget spreadsheet, you can estimate the fee income for each timekeeper in your firm. It is a simple list for each timekeeper, with their estimated billable hours for the year multiplied by their average realization rate. Your financial software may be able to run this realization report for you – if it does not, you can estimate a fairly accurate number by looking at the timekeeper’s previous history and dividing their fee receipts by their billable hours. If your firm has any contingency matters, don’t forget to account for them as well – some may be at a stage where there is guaranteed income to the firm, and some may still be truly contingencies – you should account for the contingencies in a separate line item that is not counted on.

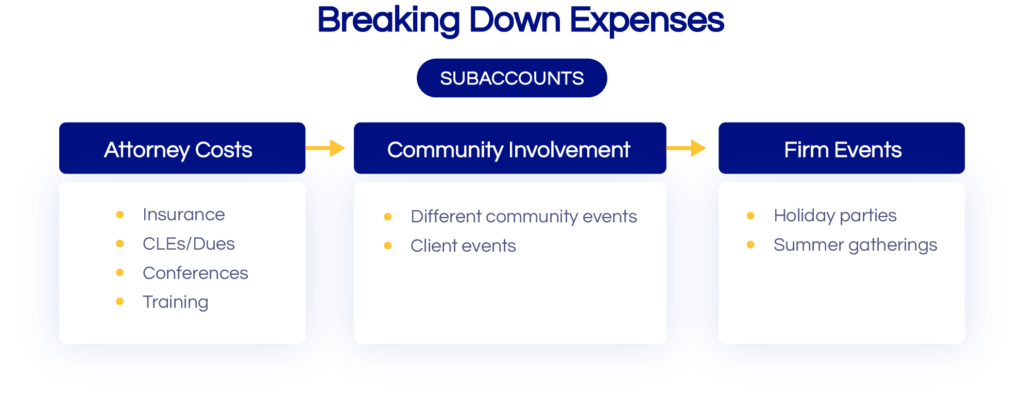

When it comes to budgeting for your expenses, be sure you have a good plan for your GL accounts before you start. Try to anticipate everything you may want to be able to track in the future. Your financial software should allow you to have parent accounts and sub-accounts. For example, you may have a set budget for firm events for the year, but you may want to be able to track what the firm spends on the annual holiday party v. its summer outing and its annual Administrative Professionals’ Day celebration. You can have a parent account for firm events, with sub-accounts for each of those sub-items. This will allow you to easily plan in future years by having a quick picture of your historical spending.

Another great way to use sub-accounts is to track costs the firm incurs for each attorney. Examples include insurance, association dues, CLEs, conferences attended, etc. By creating a sub-account for each attorney, it is very easy to run a report from your financial system to track their direct costs when you want to determine their true profitability for the firm.

When you have completed your income and expense entries into your spreadsheet, ensure that you end up with the desired net income at the end. If you don’t, you need to sharpen your pencil!

When it comes to entering your budget into your financial system, be sure you are entering the expenses in the month that you expect them to occur. Some items will be spread equally throughout the year, like rent and equipment leases. Others will occur in specific months, like professional liability renewals and holiday parties. By planning for your professional liability renewal to occur in the appropriate month, you can have your eye on the ball in cash flow planning and avoid the extra expense of paying for financing your premium.

Use your budget for decision-making. If someone is requesting something that was not planned in the budget, is it necessary? Is it something that can wait until next year? If not, is there a way you can make up for the added expense by changing your spending in some other areas or increasing firm revenue?

Once you have entered your budget into your system, make sure you monitor it regularly. You should be running a monthly YTD income v. budget report to track how you are doing against your budget. Don’t despair if you see variances v. your budget. No budget is perfect, but by having one in place and monitoring it regularly, you can prevent any big surprises and make contingency planning when necessary.