Law firms today are finding it increasingly necessary to meet specific client needs with their invoices. If your firm is to receive payments from clients in a timely manner, it is important that your invoices communicate the information expected by each client in the format that they require. With the right software and planning on the front end, this does not have to be an onerous task.

The Basics

To begin, there are some criteria that should be included on every invoice, regardless of the invoice format or template. You want to ensure your invoices provide:

Client Contact Information.

Matter Description.

Client’s File Number, Claim Number, etc. that they may have assigned to identify this matter.

Succinct task descriptions – each entry should be short and to the point but include enough information to show value. (Think of your invoices as a marketing tool, communicating to your client the value you are providing to them with your services.)

Time spent on each entry.

Summary total by timekeeper – number of hours spent, rate, and total cost.

Disbursements.

Total invoice.

Ensuring Accuracy with Attorney Time Entry

Research shows that time not kept concurrently results in as much as 30% of billable time lost. By using a system that provides a timer and ease of use for time entry, attorneys can easily track their own time in the billing system as they are working, ensuring both efficiency and accuracy of your billed time. With user-friendly software, it is no longer necessary for attorneys to handwrite their time entries, with a staff person paid to take the time to enter those tasks into your billing system.

Not to mention, attorneys can utilize technology that will allow them to automatically capture time throughout their day without missing a beat. Whether they're texting a client about an upcoming meeting, sending documents over email, or answering a call after hours, every second is automatically captured and converted into a time entry.

The Importance of Billing Templates

By using software that allows the use of multiple billing templates, your firm can create templates to meet each individual client’s needs. While some clients will pay your invoices regardless of the format (as long as the information is communicated clearly), if you have corporate clients or represent insurance companies, you will find you have many that have specific requirements. By assigning the appropriate billing template to each matter on setup, you can ensure that each client is automatically receiving their invoice in the format they require.

Additionally, make it easy for your clients to pay you directly from their bill. Think about all the bills your clients pay on a monthly basis... from utilities to internet and wifi, cellphone, the list goes on and on. And then when you think about how people are paying these bills, you'll come to find that a majority of them are being processed online electronically. So meet your clients where they already are and offer credit card payments of eChecks. Some of your clients may prefer snail mail and that's okay, but the world is trending digitally, so it is becoming best practice to offer both payment methods.

Reducing Human Error with Pre-Bill Templates

Do you have clients who have billing requests beyond the formatting of their invoices? For example, if you typically email invoices but you have some clients who require their invoice to be mailed, how does your billing staff remember this each month? By setting up pre-bill notes in your matters and using a pre-bill template that will show those notes, when your billing staff is ready to run the final invoice, they will have that information directly in front of them.

Other information that may be included in pre-bill notes is whether there is a special agreement for the matter – is it a flat fee, a contingency matter, or does it have a fee cap? How about a budget? By including all of this information in a way that it will show on the pre-bill, you will save your staff time (and therefore the firm money) while also ensuring that special agreements with clients are not missed.

The Takeaway

You can meet your client needs while also working smarter, not harder, by having specific templates assigned to each matter and tracking time in the billing system concurrently. Invoices can then be generated efficiently and painlessly at the end of each billing cycle, improving your law firm's cash flow and resulting in prompt payment from happy clients.

Law firms who wish to work for insurance carriers or larger companies are finding it almost impossible to do so if they are unable or unwilling to practice LEDES e-billing. For the firm manager who has never dealt with LEDES e-billing requirements, the task can feel daunting. With a basic understanding and a few tips to get your invoices approved through the audit process, your firm can accept clients who require e-billing without fear.

What is LEDES E-billing?

LEDES stands for Legal Electronic Data Exchange Standard. This billing format was created in 1998 to address e-billing issues. It creates uniformity among all law firms to assist corporations and insurance companies in processing and comparing law firm invoices.

How does LEDES work?

The LEDES process requires firms to use a defined set of Uniform Task Codes (UTBMS). There are different sets of UTBMS codes used for different matter types. The most common set used is the Litigation Set, but there are also sets for Workers Compensation, Counseling, Projects, and Bankruptcy, for example. Full detail of the code sets can be found on theAmerican Bar Association website.

What do Law Firm Managers need to know?

For starters, you need to ensure that the task codes used for each billing entry come from the UTBMS code set for the practice area in which you are billing (typically the litigation set). Some firms require their timekeepers to enter the codes as they enter their time entries; other firms allow their timekeepers to enter a normal billing entry, and the billing department will edit each entry at the time of billing review to include an appropriate task code.

Your invoices will need to be created in a LEDES format which will allow the invoice to be uploaded into the e-billing system that your client is using and be read on the receiving end. These invoices are uploaded to a third-party administrator’s site. There are several third-party administrators (TPAs) out there, and you may find that you have different clients using different TPAs. Your invoice will first be audited by the TPA, and they will review your entries for acceptability before releasing them to your client.

It is important to understand that the TPA is going to analyze every entry, looking for entries they can reject as unacceptable. You want to start by reviewing your client’s billing guidelines very carefully to have a full understanding of what their billing requirements are, what they will pay for, and what they will not pay for. Many clients who bill under this format are unwilling to pay for some firm expenses. For example, items like postage, photocopies, and online research may be considered by the client to be operating expenses that they will not reimburse.

The firm administrator or billing supervisor should review your LEDES pre-bills very carefully prior to submitting your invoice so that you can avoid rejections. Items to bear in mind include:

No block billing. Every task needs to be its own entry on your invoice. Part of this process includes the TPA and client wanting to see the amount of time billed for every task; accordingly, you cannot have two tasks combined in one entry.

No clerical tasks. Paralegals need to ensure their entries make it very clear that the task they are performing is legal in nature and could not be completed by an administrative assistant.

No paralegal tasks performed by attorneys. Attorney entries need to show that the task was such that it could not have been performed by a paralegal.

What happens after your invoice has been uploaded?

You will receive an email from the TPA indicating whether your invoice has been accepted. This does not mean that it has been approved at this stage, it just means it has passed the first hurdle. There are several items that could cause your invoice to be rejected at this stage:

There are timekeepers on the invoice that have not been added to the TPA’s system. Any time you add an attorney or paralegal to a client’s matter who has not billed the client previously, you need to ensure you have added that timekeeper into the system so the TPA recognizes who they are and what their accepted billing rate is.

The rates billed do not match accepted rates. If you inadvertently billed a timekeeper at the incorrect rate, the system will kick it back.

The invoice beginning date includes a date that has been billed previously. While you may not enter a beginning date as part of your “normal” billing process, for LEDES billing you must enter the beginning date of the invoice, and it must fall after the ending date of the last invoice on the matter.

Missing UTBMS codes. Any entries on the invoice that do not include a task code that is included in the UTBMS code set will cause the invoice to be rejected.

Once your invoice has been accepted, it will be reviewed by the TPA. Each entry is analyzed. Any entries that show block billing, clerical work, or attorneys performing paralegal tasks will be rejected. You will need to watch for your invoice to either be approved or have entries that have been rejected. If entries are rejected, you have the opportunity to appeal that decision. You need to follow the protocol for the TPA’s system to appeal or accept the rejections. If they are claiming something is clerical in nature, you may be able to appeal the decision and provide more detail to show why it is not clerical. You may decide they are correct in their rejection and accept the rejection of that entry.

Once the process has been completed and you have final decisions, you will want to write down the invoice balance due in your billing system to reflect any rejections that you have accepted.

How can technology help?

Your time and billing system should be set up with the UTBMS codes already in place. It should also have templates available for you that create your invoices in the required LEDES format automatically.

While LEDES e-billing can feel overwhelming at first, with some understanding of the process and the right time and billing software in place, you can accept clients with confidence that you can successfully meet their billing requirements.

The legal billing process can be a challenge for every law firm, but it doesn’t have to be. A combination of the right policies, procedures, and technology can be used to stay on top of attorney time and make the billing process efficient and accurate.

Software that encompasses both practice management and time and billing in one platform is an effective way to keep everyone on the same page and meet your clients’ needs. Use your firm’s legal software and good policies and procedures to:

Set up a client onboarding process that is consistent, seamless, and gives your new client confidence in your firm;

Ensure that all of your attorneys and paralegals are following your firm’s protocols so that you use your billing process to communicate value to your clients with accurate time entries, and make the end-of-month billing process efficient and painless.

Client Onboarding

Your law firm’s billing protocol should start with your client onboarding process. Using your practice management software, create a standardized client intake form that captures all of the necessary information upfront. It is important to set appropriate expectations from the start. Once the client and attorney have agreed on a budget and a billing rate, an engagement letter should be sent to the client for signature to ensure all parties have acknowledged in writing what is included in the representation and what the fees will be for that scope of work. Best practice steps include:

Attorney speaks with the client and comes to an agreement on the scope of work and cost.

Assistant sends engagement letter (EL) to client and calendars a task in the practice management system to ensure a signed EL is returned by the client.

Assistant notifies attorney when signed EL is returned so that work may commence. (It is risky to start work before that signature comes back – clients sometimes change their minds!)

Law Firm Billing Policy

Once the client has been engaged and you have received the returned EL (and a retainer payment if one was requested), it is time to get to work. Your firm should have protocols in place that set clear expectations for your attorneys with regard to posting their time to your time and billing system promptly. Research shows that up to 30% of fees are lost when time is not captured concurrently. Best practice steps for a firm billing policy include:

Create and communicate a timekeeping policy and ensure it is supported by leadership.

Give proper training, including do’s and don’ts/time entry examples for your practice. Time entries should be succinct with enough information to show value without being overly wordy.

Require concurrent timekeeping.

Use a user-friendly time and billing program. A cloud-based system will help your attorneys to capture time no matter where they are.

Teach your attorneys to use your billing system’s timer.

Provide your timekeepers with weekly MTD reports on their posted time to keep them from falling behind.

Provide appropriate non-billable task codes for capturing tasks such as business development, internal meetings, training, etc. so that everyone can see where their non-billable time is going.

Law Firm Billing Codes

Some clients require LEDES e-billing, and it is important that your time and billing software support this requirement. The American Bar Association has created a Uniform Task-Based Management System (UTBMS) that allows large clients (typically insurance companies, but sometimes large corporations), to track the work their law firms are performing by task. The Litigation Code Set is most often used, but there are other sets for Counseling, Project, and Bankruptcy Codes as well.

For your clients who use the LEDES e-billing practice, it is important that your time entries are drafted very carefully. Your invoices will be reviewed by a third-party administrator who is looking for anything that appears to have the potential of being an uncovered activity. Best practice steps for LEDES e-billing include:

Ensure you use the UTBMS task codes for your time entries. You may require your timekeepers to enter these themselves, or you may have a billing clerk handle the entry of all of the appropriate codes when it is time to review pre-bills.

Train your paralegals on the importance of very accurate billing descriptions that do not sound clerical in nature.

Train your attorneys on the importance of very accurate billing descriptions that do not give the appearance of being a task a paralegal could have performed.

No block billing. Zero. If you receive an email and you respond to an email, it requires two separate entries.

Someone in your billing department should review these pre-bills carefully prior to submittal to try to avoid time entries from being rejected.

If you do receive a rejection for time entries, you can appeal the decision with more information, but it is much easier and more efficient to avoid this process by getting things right from the start.

Be sure to read your client’s billing instructions carefully. Each client will have different billing guidelines. Many will not pay for what they consider to be operating expenses, such as online research, postage, and photocopies.

Billing Your Client

When it comes time to send your clients their invoices, if your attorneys and paralegals have kept accurate, concurrent time and they have followed your firm protocols for time entries, the billing process should be painless. Your time and billing software should allow you to have a billing template that is specific to your firm. Some software will allow you to review invoices in the pre-bill state within the system, where partners can review the pre-bills, forward questions to timekeepers on their time entries, and release the pre-bills to be invoiced when questions have been answered. Best practice steps in the billing process include:

Firm manager reviews pre-bills for accuracy in billing rates, client disbursements, and overall appearance.

Responsible partner reviews pre-bills to ensure time entries are accurate and communicate value to the client.

Firm manager or billing clerk processes pre-bills using firm’s billing template to submit invoices to clients.

Take a Breather (Until Next Month!)

The monthly law firm billing process does not have to be painful. With the right technology and a few policies and procedures in place, your process can run smoothly and you can have accurate invoices that show value your clients are willing to pay for.

How are changes in today’s climate impacting your law firm profitability? Technology has changed our world significantly, and law firms are slowly catching up to the rest of the business world in many areas. Gone are the days of the large offices, where every attorney has their own secretary, and the firm houses a large library full of books that must be manually updated with those supplements that would arrive on a regular basis, much to our chagrin.

As we have slowly joined the rest of the world in the ways of online research and paperless offices, we are also considering more appropriate ways to look at profitability. This is due, in part, to client demand. Clients no longer accept the idea that they will pay our firms by billable hour, with no budget or foreshadowing of what their final out-of-pocket expense may become. Technology allows for broader communication and stiffer competition, and if we want to remain competitive, we must become more efficient and readily able to consider alternative fee arrangements (AFAs) such as flat fees, risk collar agreements, etc., or at the very least, offer accurate budgets that clients can count on so that they know their worst-case scenario.

While we may have given in to the fact that we must agree to these terms in order to get the work, many firms find themselves no longer profitable as a result. Where they are falling short is in the failure to recognize that, like other businesses, they must have a cost accounting model that allows them to understand what their cost is for producing the client’s product before they can agree to a sale price.

If you think only manufacturing companies can use cost accounting methods in their businesses, think again. Law firms who are using these methodologies will leave behind those who don’t educate themselves in these practices. You may not be producing widgets, but you are selling a “product” (time) that can be measured in order to determine the cost to produce that product. By implementing a cost accounting system, you will be able to determine profitability by producer, department, office, client, and matter. (You may be surprised to learn that your largest fee income client is not necessarily the largest contributor to your bottom line!)

Determining the Cost of Your Product

So how does a firm determine the cost of their product? It isn’t as complicated as you may think. By determining the direct costs of your timekeepers (salary, payroll taxes, insurance, training, etc.) and allocating the remaining firm overhead to your timekeepers (how the overhead is allocated to differing timekeepers is another article in itself), you can determine an annual cost per timekeeper. By then looking at the number of hours each timekeeper bills per year, you can determine their hourly cost. (Timekeeper annual cost including overhead allocation ÷ number of hours billed = timekeeper cost per hour.)

Once you have determined the timekeeper’s cost per hour, you can readily understand what you can (and cannot) afford to offer as your billable rates and AFAs. You can determine the necessary billable rate for each timekeeper in order to meet your profitability goals, taking into account anticipated write-downs and write-offs (typically 10 percent). You will also know very quickly whether you can afford to offer a client a discount on any given invoice and still receive a profit on that work.

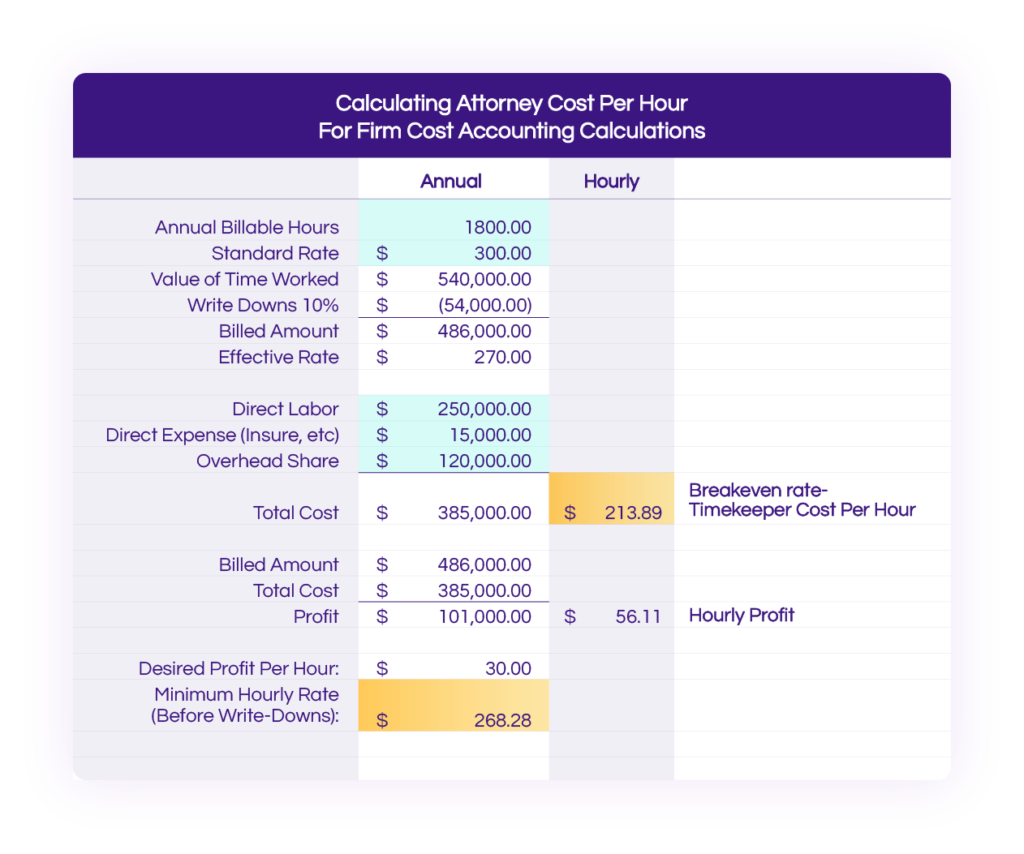

See the example below:

The attorney bills 1800 hours per year at $300 per hour, for a value of $540k.

The sample firm typically sees 10% in write-downs and write-offs, placing the true value of the work at $486k.

This puts the attorney’s effective rate at $270 per hour.

The attorney’s total cost, including their share of the firm overhead, is $385k. At 1800 billable hours per year, this puts their break even rate at $213.89.

What does this spreadsheet tell you?

You need to receive a minimum of $213.89 for each of the attorney’s 1800 billable hours just to break even on this attorney.

At the current hours, rate, and costs, this attorney earns you $56.11 per hour.

If you have a goal of a profit of $30 per hour, the attorney needs to bill a minimum of $268.28 per hour to cover write-downs and write-offs, attorney costs, and get to the desired goal of $30 per hour profit.

How does that help you?

When considering client requests for discounts on their invoices, you know whether you can afford to agree to the client request without losing money.

When considering AFAs, if you know how many hours a project should take you, you can easily come to a flat fee that will meet your desired profitability goals.

When considering whether a client is truly profitable, you know what your baseline number is. Many times our biggest clients expect deep discounts because they “pay us a lot of money.” With this information you can break it down – by looking at who your timekeepers were for an individual client, how much they billed and what their bottom line hourly rate is, you know whether the client is truly profitable to the firm, or whether they are costing you money despite the total amount they spend in fees each year.

By doing a small amount of legwork on the front end to create a model that works for your firm, you can

Ensure you are billing your timekeepers at a rate that will meet your profitability goals;

Look at the profitability of each client based on the timekeepers who have worked on their matter(s) and the effective rates for those timekeepers after receipts;

Be more accurate in your budgeting for client proposals;

Be more competitive by using this knowledge to be creative in your billing models and the use of AFAs.

One final note – be sure to require your attorneys to capture their hours, even on flat fees and other AFA arrangements. If you don’t, you will not be able to determine how successful your AFA models are working for you in helping you to maintain profitability.

What does your law firm's cash flow look like this year? How about your net income by year-end? Having a quality budget in place removes the guesswork and fear from your financial picture and ensures you end up where you want to go. We have all heard the phrase, “Failing to plan means planning to fail.” A good budget will not only help to forecast net income and cash flow, but it will help you to plan for potential problems before they become emergencies.

The two most common types of budgets are zero-based and incremental. If you are a new firm with little to no history, you will need to start with a zero-based budget. A zero-based budget is just what it sounds like – you start at zero and forecast each expense you anticipate incurring, as well as the revenue you hope to achieve.

With incremental budgeting, you have the luxury of looking back at your history and creating the next year’s budget based on what you have experienced before. Be careful though – with incremental budgeting, it can be easy to fall back on past numbers with little effort made to improve efficiencies and drill down on ways you can do better.

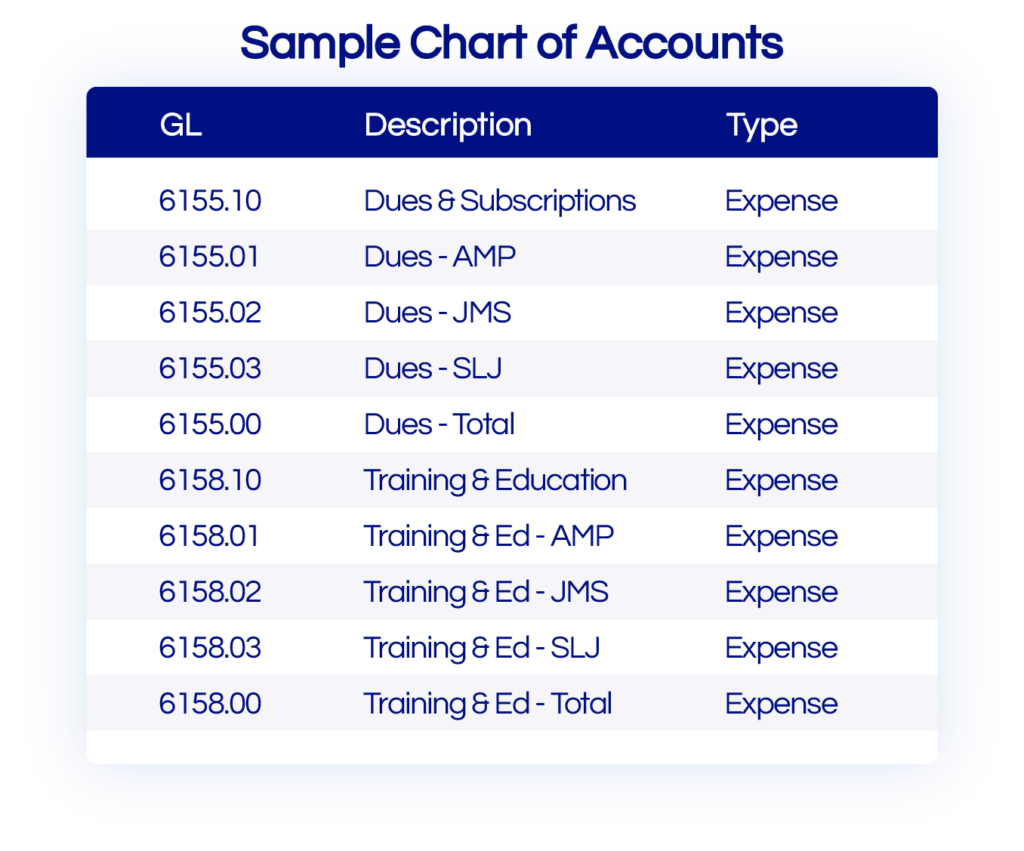

Regardless of the approach you take, the first step is to ensure you have a good general ledger chart of accounts. If you are not familiar with the chart of accounts, it is simply a list of income and expense categories used to track your spending. In a law firm, typically your income is fee income. You may also have a rental income if you own a building and rent a portion of it to other tenants. When it comes to expenses, you want to find the happy medium between having enough detail to aid you in future years without having so much detail that it is a cumbersome system to use. It is also helpful to ensure you keep any expenses pertaining to meals separate – your CPA will need to know that number at tax time because your meals are not 100% deductible!

Steps to Creating Your Budget

Step 1: Plan

Don’t plan in a vacuum. Start by reaching out to all stakeholders in your firm. What do their CLE expenses look like for the year? Any conferences planned? How is the equipment looking? Is anyone going to need any major purchases to replace outdated equipment? What about staffing? If leadership is planning to add more employees to the firm, you need to know whether you are going to have the money to cash flow that addition. Attorneys typically take six months before they show a profit for the firm.

Step 2: Insert Your Plan Into a Spreadsheet

It is helpful to use a spreadsheet for planning your budget. You should have a sheet for income, a sheet for expenses, and a sheet that links the bottom line of your total income and expenses so that you can see your forecast net income.

Begin your budget by estimating income. In your budget spreadsheet, you can estimate the fee income for each timekeeper in your firm. It is a simple list for each timekeeper, with their estimated billable hours for the year multiplied by their average realization rate. Your financial software may be able to run this realization report for you – if it does not, you can estimate a fairly accurate number by looking at the timekeeper’s previous history and dividing their fee receipts by their billable hours. If your firm has any contingency matters, don’t forget to account for them as well – some may be at a stage where there is guaranteed income to the firm, and some may still be truly contingencies – you should account for the contingencies in a separate line item that is not counted on.

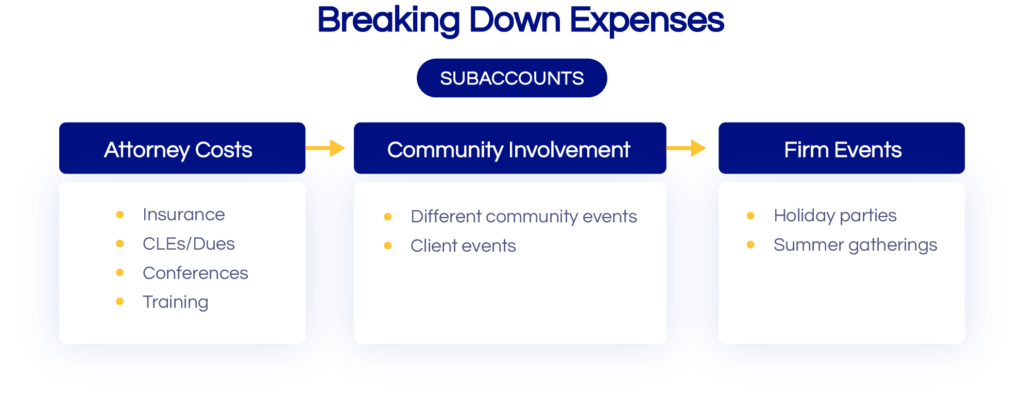

When it comes to budgeting for your expenses, be sure you have a good plan for your GL accounts before you start. Try to anticipate everything you may want to be able to track in the future. Your financial software should allow you to have parent accounts and sub-accounts. For example, you may have a set budget for firm events for the year, but you may want to be able to track what the firm spends on the annual holiday party v. its summer outing and its annual Administrative Professionals’ Day celebration. You can have a parent account for firm events, with sub-accounts for each of those sub-items. This will allow you to easily plan in future years by having a quick picture of your historical spending.

Another great way to use sub-accounts is to track costs the firm incurs for each attorney. Examples include insurance, association dues, CLEs, conferences attended, etc. By creating a sub-account for each attorney, it is very easy to run a report from your financial system to track their direct costs when you want to determine their true profitability for the firm.

Step 3: Look at Your Bottom Line

When you have completed your income and expense entries into your spreadsheet, ensure that you end up with the desired net income at the end. If you don’t, you need to sharpen your pencil!

Step 4: Enter Your Budget Into Your Financial System

When it comes to entering your budget into your financial system, be sure you are entering the expenses in the month that you expect them to occur. Some items will be spread equally throughout the year, like rent and equipment leases. Others will occur in specific months, like professional liability renewals and holiday parties. By planning for your professional liability renewal to occur in the appropriate month, you can have your eye on the ball in cash flow planning and avoid the extra expense of paying for financing your premium.

Don’t Just “Set It and Forget It”

Use your budget for decision-making. If someone is requesting something that was not planned in the budget, is it necessary? Is it something that can wait until next year? If not, is there a way you can make up for the added expense by changing your spending in some other areas or increasing firm revenue?

Once you have entered your budget into your system, make sure you monitor it regularly. You should be running a monthly YTD income v. budget report to track how you are doing against your budget. Don’t despair if you see variances v. your budget. No budget is perfect, but by having one in place and monitoring it regularly, you can prevent any big surprises and make contingency planning when necessary.

In, Accounting 101 for Law Firms we discussed how when firms are asked, “How do you want to define growth?” The leading response is always through revenue.

That is great, right?! “Revenue.” We all love this word, it’s great a great way to track performance, but how do you actually track revenue? Is it as easy as simply counting the dollars that come through your door? We wish.

The first thing you need to do is start utilizing KPIs. Your key performance indicators will be your best friends and the figures you need in order to answer the question, “how do I track my firm’s revenue?” It is important to note that these indicators are merely that, indicators. You should use them as a guide and lean on customized reports to really gain valuable insight into the productivity and performance of your firm.

At the end of the day, your firm is a business, so although you have spent 10,000+ hours honing your craft as an attorney or legal professional, you still have to be able to wear that business hat to keep the lights on.

That may sound dreadful, but don’t let the idea of numbers discourage you! These metrics can be used to help you make real-time business decisions that are going to greatly impact the future of your firm.

Profit Margin

To jump right in, let’s talk about profit margins. That is how many cents on the dollar are you able to push into your pocket at the end of the day. If it is 35%, that means you get $0.35 of every dollar at the end of the day. Your profit margin can be looked at as your net income divided by your revenue.

[cb_calculator name="Profit Margin" title=" "]

Average Rate Billed Per Hour

Next, think about how much your time is actually worth, or rather, your average rate billed per hour. This can be calculated over multiple time frames, but make sure the time frames you choose are always the same. So if you’re looking at the total hours billed for the month, don’t divide it by the total hours billed for the quarter. All of your time frames must match, otherwise, you’re comparing apples to oranges. You can calculate this amount by dividing the total hours billed for whatever time period you’re looking at, by the total dollars billed in that same period.

[cb_calculator name="AVG Rate Billed Per Hour" title=" " formula="Average Rate Billed Per Hour = Total Dollars Billed / Total Hours Billed"]

Collection Percentage

The next KPI is important: your collection percentage. You work hard week in and week out, and although you may know how many hours you billed each week, do you know how many of those hours you’re actually getting paid on? It is easy to rattle off those initial billable numbers, but the numbers you have to dig for below the surface are much more valuable. So when you’re thinking about your collection percentage, take the total cash you have collected in a time period and divide it by the total dollar amount billed in that time period.

[cb_calculator name="Collection %" title=" "]

Operating Expense Per Timekeeper

Some more advanced ratios include things like how much do you spend per timekeeper at your firm? This is very important to look at. All you need to do here is take your total operating expense that you would get from your Profit and Loss statement and divide it by the number of timekeepers at your firm. This is going to give you a really great insight into how much it costs to actually run your business.

[cb_calculator name="Operating Expense Per Timekeeper" title=" "]

Profitability by Client

Where it gets interesting is where you can use the figure you calculated from the operating expense per timekeeper to determine if you and your team are working on profitable clients. Profitability by client is huge because as you start to unpack this, you can quickly determine which of your clients truly brings your firm more revenue and which are just eating up your time. Everyone has a few clients where it costs you more to serve them, even though you may have higher billing rates. The problem with this is that most firms do not pinpoint these clients until the work is already done. So, to determine your profitability by client, simply take the fees generated by the client and subtract that estimated cost per timekeeper per hour worked.

[cb_calculator name="Profitability by Client" title=" "]

Utilization Rate

Lastly, are you hitting your targets? Your firm’s utilization is important because the more informed you can be about your productivity, the easier it will be to make decisions on matters like staff expansion. Is an extra timekeeper necessary for your growth or can you manage by simply shifting staff around? How do you determine what the right thing to do is? To calculate this utilization percentage, divide the total billable hours of a timekeeper by their total working hours. This percent may fluctuate throughout the year based on caseload, so it is important to keep your external factors in mind when making considerations for your staff.

[cb_calculator name="Utilization" title=" "]

There are many KPIs and reports you can generate and use to monitor and track your firm’s revenue. You don’t have to be a finance buff or accounting expert to do this math, and once you start incorporating it into your weekly or monthly routine, it will become second nature! Until that time, we have tried to make it as easy as possible for you to get a handle on your numbers, so we have created a KPI calculator that you can access here to get you started!

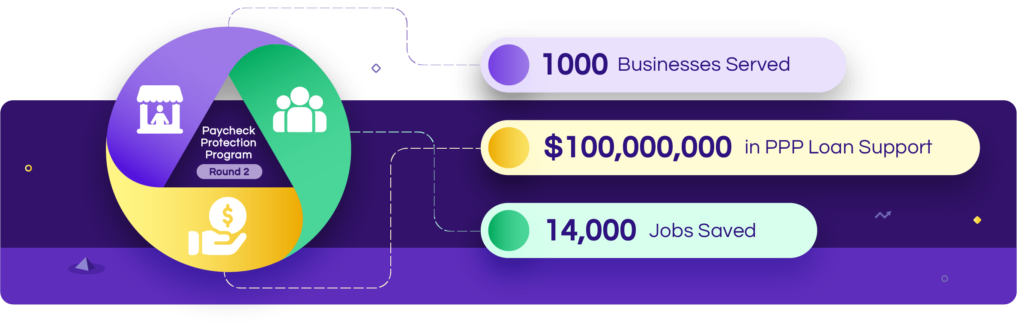

In late December 2020, Congress approved an additional COVID-19 relief package as part of the Consolidated Appropriations Act, 2021. Included in the $900 billion aid package is funding intended to provide a second round of relief for small businesses that are still struggling in the wake of the worldwide pandemic. A key piece of this legislation is funding earmarked for a second round of the Paycheck Protection Program, or, colloquially, PPP2.

The PPP Second Draw legislation is sure to be met with mixed feelings by small to mid-sized law firms across the country. Many of them are still weary from the first round of PPP; a poorly executed program that was full of uncertainties, constantly changing regulations, and a mixture of dread and uneasiness over the ramifications of improperly complying with rules that were released irregularly and without clear guidance. In fact, up until late December, one of the largest areas of concern – the tax treatment of the funds – left many law firms with cash-based, calendar-year financials with little time to plan or to react.

So now the question on law firm leaders’ minds is, understandably, “Should I even apply for PPP2?” Followed closely by, “If so, what’s in it for me?”

Here’s a quick rundown of what can be expected:

First Things First: Am I Eligible?

In order to be eligible to receive a Second Draw PPP loan, your firm must have experienced a revenue reduction of 25% or greater in 2020 relative to 2019.

This reduction can be calculated by comparing either one individual quarter from 2019 to the same quarter from 2020 or by comparing the calendar year 2019 to the calendar year 2020.

So, for example, if your gross revenue in the 2nd quarter of 2019 was $500,000 your gross revenue in the 2nd quarter of 2020 would need to be less than $375,000.

By giving firms the flexibility to compare one quarter versus another, even if you ended 2020 without a significant revenue reduction compared to 2019, you may still be eligible based on the performance of a single quarter.

Please also note that the maximum amount of any loan is $2 million and loans less than $150,000 will have easier paths to approval.

Next: What is the Same?

If you lived and breathed the first round of PPP Loans, many of the characteristics of the Second Draw PPP Loan will look very familiar to you:

Calculating Your Loan Amount

The formula for calculating the amount of your loan will be 2.5 times your average monthly costs. Average monthly payroll costs can be calculated using the 12 months prior to your loan for either the 2019 or 2020 calendar year. Payroll costs above $100,000 for any one employee (on a prorated, monthly basis) must still be excluded;

Substantiating Payroll Amounts

The documentation required to substantiate your firm’s payroll cost will generally be the same as what was required for your first PPP loan.

Maintaining Operations

Employee and compensation levels are maintained in the same manner as required for the First Draw PPP loan.

Forgiveness Terms

If your loan is not forgiven it will carry an interest rate of 1%, a maturity of 5 years, and payment deferrals.

Usage of Funds

At least 60% of the proceeds must be spent on qualifying payroll costs.

What has Changed?

While there have been a few changes there are a few unique terms of PPP2 which many law firms will find very favorable.

Covered Period Changes

Due to the top-heavy compensation models of most law firms many found themselves at a disadvantage when the 8-week covered period was first announced. Conversely, the 24-week covered period became administratively burdensome and left outstanding debt on the financials longer than many firms were comfortable with. However, the CAA now allows the borrower to select their own covered period as long as it is more than 8 weeks and less than 24 weeks from the loan origination date;

Eligible Expenditures

While PPP2 does still require borrowers to use at least 60% of the proceeds on payroll costs, the CAA has expanded the list of qualifying expenses that can result in forgiveness. In addition to items such as coverage for property damage, allowance of expenditures associated with costs outlaid for adapting your offices to meet enhanced safety standards or purchasing PPE for employees/clients/vendors, recipients can also include costs outlaid for “covered operations expenditures” to their forgiveness applications. This is defined as:

A payment for any business software or cloud computing service that facilitates business operations, product or service delivery, the processing, payment, or tracking of payroll expenses, human resources, sales and billing functions, or accounting or tracking of supplies, inventory, records and expenses;

Further, the CAA does not delineate what time period that software payment may or may not cover. So, for example, it can be assumed that a one-time payment for a year of subscription-based business software would be eligible for forgiveness if it is made during the covered period.

Tax Treatment

Unlike the uncertainty that surrounds the tax treatment of the first round of PPP, the COVID-Related Tax Relief Act of 2020 (COVIDTRA- a piece of the CAA) has stipulated, from the onset, that funds received from the Second Draw PPP will not be taxable income to the recipient and that your firm can deduct expenses that are paid for with the loan’s proceeds. Finally, borrowers will not have to reduce tax attributes (such as the NOL carryover or a capital loss carryover) when the loan is forgiven.

Two more important items to note:

Lender Selection: Even if you were unhappy with your bank’s initial rollout and administration of your first PPP loan, sticking with your original lender may mean you have less paperwork to submit thereby reducing your application time significantly and

Deadline: The last day to apply for and receive a PPP loan is March 31, 2021.

So, while you may not be ready to tackle this “beast” again, it could provide very favorable funding options as you march your firm into 2021.

And we know this process can be daunting, so we have tried to make it a little easier for you to keep your firm organized. Download this prep-list and stay one step ahead!

Prior to 2020, if your firm paid freelancers, contractors, or other non-employees $600 or more during the year, a 1099-MISC would be issued and sent to the payee.

In 2020, the IRS released form 1099-NEC, a new form that will change the way 1099-MISC reporting has been handled for years.

This 1099-NEC was added specifically for reporting non-employee compensation. This will include payments to individuals who are not employees, as well as payments for services to partnerships, estates, or, in some cases, corporations (such as attorneys and law firms).

Yes, the 1099-MISC is still being used, however, it has been redesigned, so it will be especially important to pay close attention to how payments are being reported in early 2021.

Let's take a look!

New Changes

To start, let's talk about what exactly has changed. To help give you a better visual, below is a chart indicating what exactly has changed between the 2019 form and the 2020 forms:

Any payments in 2020 to attorneys and/or law firms for services rendered should now be entered in Line Item or Box 1 of form 1099-NEC. Gross proceeds, such as settlements paid to attorneys/law firms, should now be recorded in Box 10 of 1099-MISC.

It will be more important than ever to review all vendor settings to ensure that 1099 vendor payments are reported in the correct box and on the correct form in 2020.

Form 1099-MISC must be filed by March 1, 2021, if filed on paper, or by March 31, 2021, if filed electronically. But vendor record review should begin as soon as possible because the 2020 accelerated due date for filing form 1099-NEC with the IRS is on or before February 1, 2021, whether you're using paper or electronic filing procedures.

A best practice to prevent the beginning of the year scramble to obtain missing information from vendors is to require a current W-9 prior to issuing any payments to vendors. This will ensure that each vendor record is set up properly in the accounting system. Further, an updated W-9 should be requested at the beginning of each year, prior to issuing any additional payments, to confirm that the information contained in the vendor record is accurate from year to year.

If you're using a legal practice management software, records and data may look different, but in Centerbase, each vendor has its own record where settings specific to that vendor are located. This makes reviewing and editing the vendor’s 1099 settings a very simple process. Additionally, documents such as the current W-9s can be attached and notes can be entered on a vendor record, making verification of 1099 information quick and easy.

Remember that any credit or debit card payments to vendors should be excluded in what is reported to the IRS since each credit card company (payment settlement entity) reports payments via credit card to vendors on form 1099-K. If credit card payments were to be included in the amounts reported on 1099-MISC or 1099-NEC, it would result in the reporting of the vendor’s income to the IRS twice. This may ultimately result in the necessity of filing corrected 1099’s if requested by the vendor. Centerbase provides the ability to filter out credit card payments from the 1099 vendor report, eliminating the necessity of manually reviewing all vendor payments. This report can be downloaded and used to prepare 1099’s each year.

The Takeaway

Preparing for filing 1099’s is going to take some additional effort in early 2021, specifically as it relates to legal settlement accounting. With the filing deadline for form 1099-NEC only 31 days into the new year, getting started on vendor review as soon as possible will be essential.

Now that you are armed with the knowledge of the changes to 1099-MISC and what is to be reported on the new form 1099-NEC, you should be able to accurately conduct 1099 reporting for 2020.

For more detailed information regarding 1099-MISC and 1099-NEC reporting for 2020, check out the IRS instructions.

For many firms, accounting is a huge pain point. It’s time-consuming and tedious, but it’s crucial to any business’s operations.

But before we get into the nitty-gritty, what does it even mean to close out a firm’s books? Keep reading and we’ll tell you!

Closing a firm’s books is the process of finishing up all accounting activity for an accounting period and ensuring that the general ledger accurately reflects the financial activities of the firm.

There are many closing procedures that should be followed on a regular basis throughout the year, but there are also additional procedures to include at year-end. We know, that’s just adding more to your plate, but these year-end procedures should be given special attention prior to closing the books for the fiscal year and we’ll tell you why.

Profit distribution can occur at any time during the year, so it is critical to maintaining a complete and accurate financial picture so that appropriate projections of net income and cash flow can be made whenever required. By establishing regular month-end procedures, your firm can better maintain an accurate financial picture throughout the year and, in turn, will ensure a smoother year-end closing of the books.

Of course, each firm is different and the procedures that are put in place will vary from firm-to-firm, but we have tried to make it as easy as possible for you and compiled a list that includes some basic, monthly procedures that your firm may find useful.

Accounting Procedures to Consider Following

1. Distribute a list of outstanding, unpaid accounts receivable that are 90 or more days past due to the responsible attorney for collection efforts.

The older the receivable, the less likely it will be collectible.

2. Ensure that all timekeepers are current with their time entries by the end of each month so that billing will not be delayed.

3. Record all incoming cash.

Ask yourself: Have all electronic and credit card payments been entered?

4. Review the Aged WIP Report to identify fees that can be billed and those that should be written off.

Centerbase Tip 1: If you use Centerbase already, check out our new AR Sweep to apply payments to client bills that have funds available through client overpayment, retainers and/or trust funds.

5. Reconcile all cash and credit card accounts, entering all unrecorded transactions.

A best practice is to reconcile all bank and credit card statements within a few days of having access to the statements to ensure balances include all electronic receipts and expenses, monthly fees, interest income, and interest expense.

6. Review and reconcile petty cash.

7. Record month-end payroll journal entries.

8. Review the Payment/Credit Allocation Details report, filtering for any credits for expenses.

Enter a journal entry for any matter expenses that were written off or discounted during the month to properly account for expenses that the client will not be reimbursing.

This is an important step that is often overlooked.

If a client will not be reimbursing the firm for a matter expense, it is necessary to reduce the Matter Expenses Advanced account (asset account) and increase the Unreimbursed Client Expenses account (expense account) to properly account for what will now be a firm expense.

9. Review liability accounts to ensure accuracy.

Are payables clearing out properly?

10. Review the Comparative P&L Report.

Are there any unusually positive or negative changes from the previous period?

If so, research why this has occurred and make adjustments if necessary.

11. Review the Trial Balance.

Do all accounts have normal balances, i.e. asset and expense accounts have debit balances and income and liability accounts have credit balances.

If not, review accounts with unusual balances for errors.

12. Prepare draft Profit & Loss Statement, Balance Sheet, and Trial Balance and provide to CPA for review and tax planning (and tax preparation at year-end).

A best practice is to submit financials to the CPA for review at least quarterly.

13. Enter any adjusting journal entries per your accountant's instructions.

14. Print and save finalized financial statements.

15. Update the closing date in System Settings to ensure no changes can be made that will affect the financial statements for prior periods.

And if you were thought that was it think again because we have more! In addition to the above, at year-end the items below should also be added to the closing procedures.

Additional Closing Procedures

1. Request that all expense reports be submitted to accounting in plenty of time for processing, so they can be paid prior to year-end.

2. Review IOLTA balances and request replenishment according to the firm’s policies so there are sufficient funds on hand to apply to client bills at the end of the fiscal year.

3. Update accounts payable.

Have all expenses for the fiscal year been entered? Pay all older vendor bills.

4. Pay down line of credit.

5. Plan for and enter any retirement plan funding.

6. Plan for and enter any year-end bonuses.

7. Budget for sufficient cash on hand and adequate line of credit for the first quarter of the following fiscal year.

8. Account for partner/shareholder distributions.

9. Enter adjusting entries for depreciation, bad debt, etc.

10.Enter final adjusting journal entries per accountant's instructions.

11. Per the Accounting Period End Date set in the Accounting System Settings, Centerbase will process the year-end closing entries to book the current year’s net income to retained earnings.

This will also $0 out all income and expense accounts for the first day of the new fiscal year. It is the final step in the year-end closing process. No prompting is necessary as it is an automatic procedure that Centerbase performs.

The Finale!

At this point, you’re either thinking “oh boy,” or “wow that was helpful!” Either way, we want to try to make this process as easy as possible for you so we have created an Accounting Period Closing Procedures Checklist to assist you in assigning and tracking the tasks listed above.

End-of-year closing is never fun, but hopefully these steps and checklist will help you keep billing, collections, and your financial records up to date!

As we draw near the end of 2020, many attorneys find themselves faced with the same universal question — “Is there any way I can collect on my outstanding receivables before the year is out?” Although it’s not something you dreamed about in law school when you thought about practicing law, collecting on unpaid bills is a vital aspect of your business. Ideally, you should want to end your year with as much money in your pocket as possible. But, how can you collect on invoices that some clients thus far have ignored or refused to pay?

First, some quick definitions. Accounts Receivable, or “A/R,” is a term that refers to unpaid balances left on a client’s account. Furthermore, an “Aged A/R” is an unpaid balance that has been left standing for a certain, prolonged amount of time (say, for example, a client has not paid their invoice in over 60 days).

Now, let’s present a common scenario: Your client emails you saying she cannot pay her outstanding invoice. In this instance, many lawyers choose one of three options: 1) hang on to the invoice and hope their client eventually pays it; 2) enlist the help of a debt collector to obtain the funds; or 3) simply write off the debt when the year is over. Option One is less than ideal, because you have no assurance of ever getting paid. Option Two is hardly ever preferred because you still want referrals from that client, and handing over their outstanding balance to a collections firm is not likely to instill good feelings between attorney and former client. Thus, the majority of attorneys end up choosing Option Three, wherein they simply write-off the debt at the end of the year.

But, is there another way to get paid on an account that you were all but ready to write off?

The short answer, for the most part, is yes! Attempting to collect on unpaid invoices is not a fruitless endeavor, no matter how aged the invoice is. Let’s look over a few quick tips to point you in the right direction.

Get organized

Naturally, every client you take on is unique in their own special way, and this also translates into their invoice payments. There is no “one-size-fits-all” solution to collect on A/R—every client with an outstanding bill will require a different strategy, but there are still some universal applications that you can utilize to track down your payments.

You can accomplish this by first creating a list of every client with an unpaid invoice, including their name, their matter number, the amount they owe, and how long the balance has been overdue (i.e., 30 days, 60 days, 90 days, and 120+ days). If you work at a firm with multiple attorneys, you could also label each invoice based on the primary attorney overseeing the case.

Once you’ve put your list together, you can then determine which invoices you should go after first. You may consider tackling the “youngest” invoices first—that is, the invoices that have gone unpaid for the shortest period of time (let’s say 30 days, for example). Set aside time in your day to email these clients with a short, to-the-point message about their outstanding invoice, including the amount they owe. Include a link for the clients to pay online - the goal is to eliminate friction between your client’s pocketbook and your bank account. From there, you could expedite the process by duplicating the email for the remaining clients on your list—simply change the names and the amount owed, and send it off. This email should come from the attorney working the case; the attorney’s email address is more likely to grab the attention of the client.

When dealing with the older invoices, you can follow a similar plan as above, at least with the clients whom you believe will pay if prompted (or will have a way to do so in the near future once you’ve reminded them). However, there is a high likelihood that you have clients on your A/R list whose ability and/or willingness to pay don’t inspire much hope on your part. These are the clients that you fully expect to write off at that end of the year.

In these cases, consider offering the clients an opportunity to wipe a portion of the debt away if they pay within a certain period of time. For example, if a client owes you $10,000.00 and has not paid you in over six months, consider emailing them with an offer that if they pay half of their balance ($5,000.00) within the next three business days, you will forgive their remaining balance. You would be surprised at how many clients will take you up on this.

Adopt online payments

Another way to turn unpaid invoices into paid invoices is to make it easier for your clients to pay you. That’s where an online payment solution can make a big difference. These solutions give you the power to email your clients an electronic invoice that they can pay with a credit card, debit card, or eCheck. Rather than having to find their checkbook, write out a check, find an envelope, and break out their stamps, your clients can pay you with a few clicks of a button.

You would be doing yourself a favor in the long run by integrating online payments into your practice. Like it or not, cash and check payments are becoming less popular in favor of online payments and credit cards, with less than half of U.S. adults carrying cash on them on a regular basis.

Ideally, you should use an online payment solution that was built with the legal industry in mind, with features that can correctly separate earned and unearned fees and protect your IOLTA account from third party debiting. You can stay compliant with your state bar and also provide a benefit to your clients at the same time.

In short, giving your clients the ability to pay online will not only entice your late-paying clients to pay their invoices, but will also entice future clients to seek your services by giving them the payment options they most commonly use for most every service in their daily life.

This is only a cursory look at some of the strategies you could employ to get more cash in the door before the year’s end. If you’re looking for a deeper dive on collecting unpaid invoices from clients by the end of 2020, read LawPay’s latest e-book, Finish Strong: How to End the Year on Better Financial Footing. You’ll discover essential steps to keeping your cash flow strong at the end of your year, and you’ll leave with the right tools to reduce your outstanding receivables going forward into the new year.

Jordan Turk is a practicing attorney in Texas, and is also the Legal Content and Compliance Manager at LawPay. She earned a B.A. in Classics, History, and Religious Studies from the University of Texas, and went on to earn her law degree from the University of Arkansas School of Law. Prior to LawPay, Jordan worked with a high-asset family law firm in Houston, Texas.

Here’s a quick rundown of what can be expected:

Here’s a quick rundown of what can be expected: