Get a Free Demo

By Debbie Foster, CEO, Affinity Consulting Group

Law firm profitability is often viewed in simplistic terms: the more billable hours attorneys log, the more profitable the firm becomes. But the reality of assessing profitability is far more nuanced. Profitability can be sliced and diced in several ways — by practice area, client, lawyer, and matter profitability, and more — and your firm has to determine what’s appropriate to analyze.

That can get complicated, but my goal with this article is to help make profitability analysis feel doable by looking at just one example — practice area profitability. We’ll look at how you can use practice area information to make strategic decisions about resource allocation, maximizing your profit margins, and maintaining a healthy work environment for your attorneys and staff.

Before we can begin analyzing profitability by practice area, we must understand what it costs your firm to provide its services by determining each attorney’s cost rate.

This is essentially the hourly cost of employing them, including salary, benefits, and overhead expenses such as office space and technology. This rate forms the foundation for assessing whether your firm is pricing its services appropriately and whether each attorney is contributing to overall profitability.

Calculating attorney cost rates involves several components:

Calculate the cost rate for each attorney by adding their salary and benefits to their share of overhead expenses. This will give you a baseline cost per hour for each attorney, which can then be compared to their billing rate to determine their contribution to profitability.

Now that you’ve established attorney cost rates, you're ready to analyze profitability by practice area. This is often a relevant category to assess within a firm because it can reveal valuable insights that might not be apparent from a high-level overview of your firm's financials.

For example, a firm may appear profitable overall but harbor unprofitable practice areas that are being subsidized by more successful ones. This situation can lead to resentment among partners and potentially affect staff retention.

Not all practice areas are created equal — some may generate substantial revenue but come with high costs, while others may be highly efficient profit centers.

You can understand practice area profitability at both a high level and a granular level. By breaking down profitability by practice area, firms can identify which areas are driving the most profit and which may be underperforming. Here are some guidelines to approach this analysis:

You want to regularly assess the profitability of each practice area by tracking revenue, costs, and utilization rates. Adjust resource allocation to ensure the right attorneys are working on the right matters to maximize profitability.

Another crucial factor that impacts profitability is how work is allocated across the firm. The concept of “highest and best use” can help ensure that the right person is doing the right work at the right time. This is particularly important for maximizing profitability in practice areas with mixed levels of complexity.

Conduct regular reviews of workload distribution to ensure that partners, associates, and support staff are all working at their highest and best use. This will help optimize profitability while maintaining a balanced workload across the firm.

Benchmarking plays an important role in understanding whether your firm is performing as well as it should be. You can benchmark against both internal and external standards to identify areas for improvement and set realistic goals for growth.

Use benchmarking data to set performance targets for practice areas and individual attorneys. This will help create accountability and ensure that everyone in the firm is aligned with profitability goals.

Maximizing profitability requires moving beyond increasing billable hours to taking a holistic approach. This should include understanding attorney cost rates first, and then analyzing a category that makes sense for your firm, such as practice area performance. With this combined cost rate at practice area data, you can begin allocating resources strategically — all to identify hidden opportunities for growth, make data-driven decisions, and ensure long-term profitability for the firm.

By Paige Roncke, Chief Revenue Officer, Centerbase

The legal industry is at a critical inflection point where law firms can no longer identify only as legal services providers. Law firms must also be data and technology companies in order to effectively compete in the market for long-term success.

I discussed this new landscape with Debbie Foster, CEO of Affinity Consulting, during a webinar on law firm profitability. A substantial portion of that conversation was rooted in the theory that profitability is more than a simple math formula of revenue minus cost; rather, it’s about understanding your firm's opportunity to maximize revenue streams while also minimizing costs without compromising quality of legal services.

It’s a misnomer to assume the application of technology only minimizes cost. Yes, technology has a critical role in automating administrative tasks, optimizing billing processes and creating comprehensive and speedy communications both internally and externally. However, technology is best utilized when the full power of software is applied to maximizing potential revenue streams.

This can be software-driven enhancements like improving time capture to create more billable hours, building reports that provide deeper insights into profitability at various levels — from individual attorneys to entire practice areas — through data clarity and availability, and utilizing that data to retain and attract stronger talent that can bill at higher rates.

In other words, as Debbie stated, “Technology should be used as a revenue multiplier.” And multiplied revenue leads to greater profitability.

While many firms have already made investments in technology, they may not be fully utilizing these tools. Let’s examine how technology can enhance law firm profitability by improving time tracking, managing billing, and providing actionable insights into the firm’s financial health. We'll also discuss common technology pitfalls and how to avoid them, so your firm can make the most of your technology investments.

With the right tools, firms can unlock efficiencies that translate directly into higher profits. The key is knowing how to leverage technology effectively to improve law firm profitability, such as:

Despite these opportunities to use technology as a revenue multiplier to drive significant profitability gains, many firms struggle to fully leverage the tools they have — and that often leads to cutting technology costs. But cutting costs isn’t a sustainable path to profitability.

Consider these common pitfalls to avoid so you can maximize your technology to advance your revenue streams.

Many law firms invest in technology but only use a small fraction of the available features. For example, your firm might not be taking full advantage of your practice management software’s time tracking, billing, and reporting features that could improve efficiency. Leveraging a tool’s full capabilities can not only improve efficiency but help reduce stress at work, too. Encourage continuous learning, where attorneys and staff explore new features and share tips for improving efficiency.

Too often, technology implementation is treated as a one-time event rather than an ongoing process. A lot of effort goes into the rollout and not enough into continuous training to learn about the tool after it’s been implemented.

As Debbie says:

“We really need to marry up our technology spend with building a culture of training.”

Pay attention to new updates and features, and make sure your staff learns how to use them by providing ongoing training and support. Consider hosting monthly lunch-and-learn sessions to discuss new ways to use your tools more effectively.

One of the best things technology can do for your firm is standardize processes. Sure, every lawyer prefers to do certain things differently, but technology can help you agree on standardizing core elements of practicing law and running a firm. The result goes beyond efficiency.

New associates coming out of law school want to gain experience with modern technology — and they expect it. Maximizing your technology presents your firm as forward-thinking and committed to providing resources to work effectively, and that can help you stand out as an employer of choice.

Newer technology presents employees with an enhanced user experience with fewer clicks, simpler and more modern interfaces, and intuitive ease of use. This streamlined experience over older systems leads to higher job satisfaction, boosting your talent retention and attraction.

Technology is no longer optional — it’s essential for creating a long-term competitive edge. Whether it’s automating time tracking, streamlining billing, or analyzing profitability across practice areas, the right tools can make all the difference in how efficiently your firm operates.

By embracing technology and ensuring it is fully integrated into your firm’s processes, you can unlock new levels of profitability, improve client satisfaction, and future-proof your business for years to come. The key is not just investing in technology but leveraging it to its full potential—and continuously improving how you use it through ongoing training and fostering a culture the embraces technology.

Profitability is one of the most critical measures of success for any law firm. But while it’s easy to fall into the mindset of “more billable hours equal more profit,” the reality is more complex. Simply focusing on the standard math equation of revenue minus expenses equals profitability doesn’t always tell the full story of a firm’s financial health.

In a recent webinar, “The Next Generation of Law Firm Profitability,” Debbie Foster, CEO of Affinity Consulting, and Paige Roncke, Chief Revenue Officer at Centerbase, explored the essential components of law firm profitability, moving beyond the basic math to consider how different practice areas, lawyer cost and billing rates, client profitability, revenue generation, and cost management play a crucial role.

At a foundational level, profitability is calculated as revenue minus expenses. It's a straightforward equation, but there are multiple factors influencing law firms’ revenue and expenses.

“While the simple math for profitability is accurate,” Debbie says, “in law firms, we need to look beyond what the profitability number is to what the profitability number could be in order to maximize what is left.”

To do this, you can define your firm’s profitability inputs by considering:

“There are many ways to look at profitability, so you have to double down and figure out what combination of these inputs makes sense for your firm, and how will you track it,” Debbie suggests.

Let’s take a look at where to start.

To move beyond the basic profitability equation, analyze the underlying factors that influence both revenue and expenses at your firm. By doing so, you can identify opportunities to maximize profits and make data-driven decisions. Here are five key areas to assess in your firm.

Each lawyer in a firm has a different billing rate and cost structure. Partners might bill at a higher rate, but they come with higher compensation. Associates, on the other hand, may have lower billing rates but can be profit centers if their work is leveraged effectively.

Take the time to figure out each of your lawyer’s cost rate — what it costs them to provide their services — factoring in their salary, benefits, office space costs, and technology costs. By calculating this cost, you can determine the minimum amount each lawyer needs to bill to cover their expenses and contribute to the firm's profitability.

Actionable insight: Now that you know how much it costs for this lawyer to provide their services, you can better determine a billable rate that will enable profitability. Follow this method to calculate the hourly cost rate for each lawyer and compare it to their hourly billing rate. If a lawyer’s cost rate is higher than their billing rate, this could indicate a profitability problem. Ensure that work is assigned based on each lawyer's cost-effectiveness, balancing their rates with the profitability of the cases they handle.

Not all practice areas are equally profitable. Some might generate higher revenue but come with greater expenses, while others may be less lucrative but require fewer resources. For example, family law cases might involve more administrative work, while corporate law could bring in larger retainers but demand more expensive expertise.

Actionable Insight: Start by analyzing each practice area’s cost rate to determine its profitability. Track the hours billed, expenses incurred, and the average rate charged. By understanding which areas are most profitable, you can make strategic decisions about where to focus your resources and who to leverage in your firm for different types of work.

“Understanding cost structure gives insight into appropriate billing rates for attorneys within a practice group,” Paige says. “With this information, you can balance the practice area’s work, having attorneys with a lower cost rate handle work that doesn’t require a senior partner’s expertise, which starts to help you adjust your profitability for that practice area.”

Not all clients are created equal in terms of profitability. Some may require more time, resources, and attention, while others are more straightforward and generate higher profit margins. By understanding which clients contribute most to the firm's profitability, you can make more informed decisions about where to invest your time and effort.

Actionable Insight: Regularly review client profitability by tracking the time spent on each client’s matters and the revenue they generate. This will help identify high-maintenance clients who consume resources without delivering commensurate revenue, enabling the firm to renegotiate terms or focus on more profitable clients.

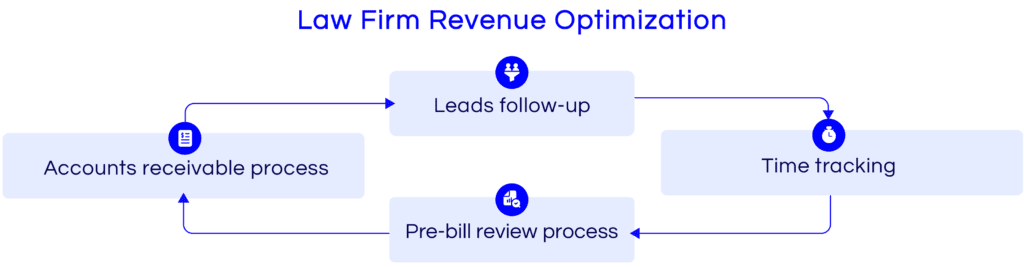

Maximizing revenue might seem like a straightforward goal, but the practical aspects of capturing all billable time, diligently following up on leads, minimizing write-offs, and optimizing accounts receivable collections often fall by the wayside. It's common to underestimate the significance of these seemingly mundane yet critical tasks that can make or break your firm's profitability.

Actionable Insight: Maximizing these revenue-generating tasks comes down to having the processes and tools in place to set your firm up for success. Paige sums up four actionable areas to optimize your firm’s revenue.

Law firms have three main expense categories — personnel, office space, and technology — and managing these costs is another important factor in a firm’s profitability. However, it’s not necessarily about minimizing expenses, but rather optimizing what you spend.

“It’s important to not waste money,” Debbie says, “and you do that by making sure you’re leveraging what you buy. You need to think about people planning, space planning, and technology planning to utilize them all effectively.”

Actionable insight: Using technology as an example, if you invest in cloud-based software but don’t review the updates and learn about new features regularly, then you’re not leveraging the software — or your money — to its full capacity. Similarly, when you hire new staff members but provide little training on the firm’s processes, technology, and culture, you’re not optimizing personnel or technology, and you’re risking additional expenses through attrition if staff members become disengaged to the point of resigning.

Understanding profitability isn’t just about looking at the revenue minus expenses equation. It’s about going beyond basic math and exploring how you can optimize each component of your business. By focusing on core drivers of profitability — cost and billing structure, practice area profitability, client profitability, revenue generation, and cost management — your firm can uncover opportunities for long-term growth and profitability.

Stay tuned for our next article, which will focus on the impact of technology and how to leverage it for law firm profitability.

Written by Carol Patterson

Law firms that solely rely on tracking billable hours might assume that each legal matter they handle is equally profitable. This assumption is based on applying an attorney’s individual hourly billing rates to the client hours they devote to each matter. But this isn’t the most accurate way to determine matter profitability.

Some types of client engagements are likely to incur significantly higher costs than others, while some matters generate greater profit margins. The only way to tell which matters the firm should invest its time in is to look at profitability at the matter level.

So, what is matter profitability, and how can you maximize it at your firm? In this article, we’ll explore the concept of matter profitability and provide practical strategies to help optimize your law firm’s financial performance.

Matter profitability refers to a law firm’s ability to generate optimal revenue and profits from each legal case or matter they handle. It’s a critical metric that directly impacts a law firm’s financial health and long-term sustainability. It goes beyond just billable hours. It involves considering various factors, such as the complexity of a matter, the expertise required to handle the matter, the resources allocated to complete the work, other expenses associated with the work, and the efficiency of the legal team.

To calculate matter profitability, law firms must deduct all the direct and indirect costs associated with handling a particular matter from the revenue that the case generates. Direct costs include attorney fees, court filing fees, expert witness fees, and other case-specific expenses. Indirect costs include overhead expenses, such as office rent, administrative staff salaries, and general administrative costs.

Fortunately, law firms can employ several strategies to improve matter profitability without compromising the quality of legal services provided. It all starts with the data you collect on your firm’s profit margins. Let’s take a look at some common scenarios for law firms and how firms can improve their matter profitability.

Matter profitability starts with selecting the right cases from the outset. Most client intake processes gather basic information about a client and their matter, but you need to do more than run a basic conflicts check and assess the facts to determine whether you should take a matter.

To identify matters that have the highest profit potential, you need to understand the types of cases that generally have lower expenses and generate the most successful outcomes. Profitability reporting data can show you historically what types of matters have been the costliest in terms of outlay, led to fewer collections, required higher write-offs, and more.

Law firms should regularly evaluate matter performance to identify areas of improvement and what cases to find to keep profitability high. Conduct post-matter reviews to assess the financial performance of each case, analyze the effectiveness of the legal strategies employed, and identify any cost overruns or inefficiencies. This feedback loop allows the firm to make data-driven decisions that will enhance future matter profitability.

The key is to remember that improving law firm profitability at the matter level requires firms to take a deeper dive than just billable hours and billing rate. Firms should run profitability reports to get greater insights into their expenses by matter and their client pay timelines so they can answer several questions:

Profitability reporting can highlight areas where there may be problems in workflows in your law firm that are inhibiting profitability, such as an attorney’s failure to enter all time worked or write off too many tasks. To understand the true cost of a case, attorneys need to understand all the time they spend on a matter, regardless of whether it is billable, and any time reductions.

As for expenses, law firms need to track both hard and soft costs. Hard costs are any costs paid on a client’s behalf. Soft costs are overhead costs, such as office leases, copying, mailing, deliveries, and the like.

Depending on what the profitability reports show, it may make sense to change how your firm bills for certain matters. In some cases, a flat fee model may not work well, and you may need to switch to an hourly rate or to a percentage of the recovery on a case. Or, if clients are not paying their bills on time, you may need to set up a payment schedule or plan. If nonbillable hours or written-down hours seem high, you should talk to the attorney responsible for the matter about why and figure out a strategy that reduces those costs in the future.

If you aren’t hitting the 50 percent profitability target at your law firm, you may be wondering which matters are really contributing to your bottom line. To get the answers you need, look to our latest tool: Profitability Reporting. With Centerbase Profitability Reporting, you can go beyond your gut and get clear, actionable insights into which matters are the most profitable and which matters to avoid, so you can seize the right opportunities for law firm growth.

Are you ready to take your matter profitability to the next level? Contact us to sign up for a demo of the Centerbase platform and our Profitability Reporting tool today.

Written by Carol Patterson

All law firms collect and study data about their bottom line. If they’re in the red, they know they need to figure out what’s holding them back. But if they’re in the black, they may not dig deeper to understand what’s working and what’s not. After all, a profitable firm is a healthy firm, right?

That’s not always the case. If your law firm has multiple offices or is practicing in several different areas of law, it might be that one location or practice is propping up another. Or it might be that a potentially profitable practice is located in an area with too few high-paying clients or with a high tax rate.

Aren’t these details you’d want to know as a law firm leader? Absolutely! And you can by using Profitability Reporting tools. Let’s take a look at some scenarios where profitability data can help you make smart, strategic decisions that will move your law firm’s profitability forward.

Our [fill in the blank] practice group or law firm location is busy, but it’s not turning a consistent profit. How can we figure out why their profitability is so low?

One reason is that you might have situated a practice in the wrong location. Let’s say you’ve got a divorce and custody practice located in a big city, where there’s lots of competition and a high tax rate to boot. You’re going to have to keep your prices lower to compete for business, and then the government is going to cut into those fees even more.

You can use your profitability data to identify underperforming locations or practice groups and take appropriate action, such as closing or merging offices or practices, to optimize profitability. With this data in hand, you can model different scenarios, including adjusting your billable rates or flat fees to accommodate a higher tax rate and take on fewer clients. Or you may need to move a practice to a satellite office outside the city and use remote tools to work with clients in the city to improve your practice group profitability. Alternatively, you might find an opportunity to acquire another law firm in that area and then focus your resources on other, more profitable practice areas.

Some of my lawyers work in multiple offices. How can I see where they’re working most profitably?

If you have a profitable attorney splitting their time between a Connecticut office and a New York office, it can be hard to tell where they’re generating the greatest profits unless you look at their results by location. The key is to look at the location where the work is actually happening.

Profitability Reporting can help you isolate where your attorneys’ profit margins are the highest, so you can sift through the details about their billed, written-off, and collected fees and their costs to drill down to the details that matter.

Our attorneys want us to spend more dollars on advertising, but I’m not sure we’re getting our bang for the buck. How can I tell what marketing strategies are working?

If your partners are blowing through their marketing budget and their profitability numbers aren’t soaring, you need to figure out why. One way to sort out what’s working and what isn’t is to run a report on profitability by resource.

Let’s say a lawyer wants to invest in advertising on a particular radio show and claims that they’re bringing in new clients based on their ads. A law firm administrator can dig into the numbers to determine the impact of that spend on actual client revenue. If the clients are coming in but not bringing the dollars with them, it makes sense to invest those marketing dollars in other channels that will lead to more lucrative business.

Some of our practice areas have razor-thin profit margins. How can I improve the profitability of these practice areas?

To accurately assess profitability, law firms need to allocate both revenue and costs correctly. This involves allocating direct costs, such as salaries and expenses directly related to specific locations or practice areas, as well as indirect costs, such as overhead expenses and shared resources.

Some of these costs may include write-offs too. Take, for example, insurance defense practices. Often, the profit margins in these practices are razor thin, given competition and the rigorous scrutiny that insurance companies apply to their bills. If you bill for the wrong thing, their billing software algorithms will identify problematic entries and send the invoice back to you, further delaying payment and shaving your profit margin even thinner.

While it’s good to offer some services pro bono, you don’t want to pay businesses to be your clients. To ensure you’re focusing your attention on profitable clients, you can look for cost savings opportunities. You can also study how much each practice area is writing off or not collecting and use it to determine whether you need to adjust your rates, change how you bill for your work, or make different decisions about who your firm takes on as clients.

Find new avenues to law firm productivity with Centerbase’s Profitability Reporting

Partners and firm administrators have a new tool in their arsenal for measuring their law firm profits: Profitability Reporting. The latest addition to our software portfolio empowers leaders to make smarter decisions about resource allocation, marketing, and more using profitability at the practice group and office location level (as well as by timekeeper). Law firms can also focus their attention on markets and practices with the greatest potential for growth, client acquisition, and revenue generation.

Are you ready to take your location and practice area profitability to the next level? Sign up for a demo of the Centerbase platform and our Profitability Reporting tool today.

Written by Carol Patterson

If you’re running a small or midsize law firm, you’re probably juggling a lot of things, trying to maintain your law practice while also managing the business of your law firm. You may not always have your finger on the pulse of the metrics that matter, yet you probably do take a quick glance at your firm’s overall revenue and your timekeepers’ billable hours. So far, your firm isn’t in the red, and your partners seem to be churning out work. But these two statistics, in isolation, aren’t a meaningful gauge of your firm’s overall performance.

Say, for example, that you have an attorney who is bringing in a ton of revenue. However, when you take a closer look at the numbers, you discover that his expenses are incredibly high, and he isn’t billing enough to cover the costs of his practice.

You might also have brought in a lateral with a huge book of business — and a huge salary to boot. But while his billables are high, there are too many write-offs to cover his monthly paycheck.

Or perhaps your star rainmaker has landed a million-dollar client. But the expenses of working for this client are sucking your firm dry to the point that you’re actually paying this client to be on your roster. You’re running a law firm, not a charity.

How can you figure out that these problems exist if you don’t look at profitability by timekeeper? You can’t.

As you can see, it takes more than managing the bottom line to run a successful law firm. And a firm’s success depends on the success of every timekeeper. That’s why it’s so important to monitor profitability per attorney or timekeeper. That’s where Profitability Reporting comes in. Here are just some of the pressing profitability questions that a good tool can help you answer.

There’s a tremendous difference between being a top biller and being profitable. If an attorney is burning the midnight oil every night churning out briefs or contracts, they may not be as productive as they should be. Clients can’t be billed for inefficient work, so some of these timekeepers are having their hours written off.

Your law firm’s goal should be a 50% profit margin. That means you should set the same profitability goal — 50% — for each timekeeper too. Profitability Reporting can show you the complete picture of how write-offs are hurting your profits.

Profitability Reporting can also help you assess the profit margins for each timekeeper by comparing their billed, written off, and collected fees to their associated costs, including overhead expenses and direct costs. If timekeepers aren’t billing enough to cover their keep — their overhead including their salary — something needs to change.

Profitability Reporting can give you the insights you need to have a coaching conversation with attorneys who aren’t logging enough hours so you can help them find ways, such as automation, to make their work more efficient; encourage them to spend less time on nonbillable matters; or balance the workload so everyone has a more equal load. You may also notice an opportunity to help lawyers struggling to meet their billable quota with tools that make it easier for them to capture every billable minute. If all else fails, you may need to adjust their billing rate, encourage them to manage their costs more effectively, or even change their salary to match their profit margin.

It may be that your lawyers are doing lower-value work or work for clients where the profit margin is razor thin. Profitability Reporting helps you evaluate the value of different practice areas and types of work that your lawyers handle. The right tool pinpoints trends and shows which areas, matters, and tasks generate higher billable hours and profit margins. This analysis can help guide resource allocation and encourage your timekeepers to search for clients and focus on the work that delivers the biggest payoff for their effort.

Timekeeper data can also show you whether you have set the appropriate pricing and fee structures for the work. By analyzing the relationship between billing rates, fee structures, and realization rates, you can identify opportunities to adjust billing rates, introduce alternative fee arrangements, or negotiate better terms with clients to improve your overall profitability.

Finally, the data in a Profitability Reporting tool can help you make tough choices. It may be that a lawyer on your team is just not able to generate the profit necessary to justify keeping them in the firm. If that is the case, it’s better to cut them loose so that your firm can focus on recruiting timekeepers capable of keeping your firm in the black.

Typically, profitability is calculated using hours worked. But if your timekeepers aren’t counting their hours because you’re billing clients on a flat-fee basis, then you can’t make that calculation. That doesn’t mean all is lost.

New Profitability Reporting modules are being built n that will help you calculate profitability even when you’re using a flat rate for your services.

Our new Profitability Reporting tool makes it easy for law firm leaders to track revenue, expenses, and profits at the timekeeper level. With this data in hand, you can determine how each timekeeper in your practice can improve and give them targeted advice to strengthen their performance. And, when each timekeeper improves, you increase your firm’s overall profitability.

The Centerbase platform gives you all the tools you need to turn your law firm into a profit-generating machine. To learn more about our Profitability Reporting tool, reach out for a free demo today.

Written by Carol Patterson

For five quarters in a row, law firm profitability has fallen, according to the 2023 Report on the State of the Legal Market, a study conducted by the Thomson Reuters Institute and Georgetown. (Data are based on reported results from 170 US-based law firms, including 46 AmLaw 100 firms, 47 AmLaw 200 firms, and 77 midsize law firms.) Profits per equity partner are down for the first time since 2009. Client payments and realization rates are down too.

Demand has also dropped for everyone except midsize firms, where clients are flocking because they want quality legal services without the major firm price tag.

So, how can small and medium-sized law firms capitalize on this demand and optimize their profitability? That’s what we’ll cover in this article.

Law firms should focus on profitability for a number of reasons. First, being profitable ensures that the firm can sustain its operations and provide quality legal services to clients. Having a profit allows firms to comfortably cover their operating expenses, such as rent, salaries, technology, research materials, and marketing, and establish contingency funds and reserves for unexpected expenses or downturns in business, such as a global pandemic, potential lawsuit, or market uncertainties.

It’s also important for law firms to have sufficient funds to invest in resources and infrastructure to stay competitive and deliver efficient services. To stay ahead of the curve, firms should make investments in technology, legal research tools, document management systems, communication tools and client portals, matter management systems, and training. The more profitable a firm is, the better it can enhance its capabilities and client service through investments like these. And the more investments a firm makes, the better able it is to attract, engage, and retain attorneys and staff members — not to mention pay them competitively.

Finally, profitable law firms are positioned to pursue growth opportunities and expand their practice areas or geographic reach. They can invest in client and business development strategies that attract new clients and increase their market share.

The baseline profitability goal for a law firm is 50 percent. If your firm isn’t hitting that mark, it may be because your expenses are too high or you aren’t earning enough revenue. Or maybe you are too heavily staffed, which can drain your law firm’s financial resources. The key is to figure out what is causing the problem.

Many firms look at their profit and loss statements, but these statements don’t tell you the whole story. The typical law firm P&L report isn’t granular enough to help you determine the true source of revenue and expenses. You may have a timekeeper who brings in a lot of revenue but not enough to cover their incredibly high expenses, for example. Or you may have a million-dollar client, but what you shell out to keep that client and maintain their business is so high that you’re essentially paying the client to remain on your roster. But you likely can’t tell that from your current financials.

The problem stems from too many law firms not running their firms like a business. Law firms that lack accountants don’t fully understand the concepts of what makes firms profitable. If your firm’s office manager or paralegals are managing your accounting, they are certainly capable of handling billing, checks, and cash receipts, but they won’t be able to focus on your law firm’s bigger financial picture.

The bottom line is that if you’re focusing just on revenue and expenses, you’re missing important details. Many law firms overreact when expenses look high and look for ways to make cuts. But if you’re focused on reducing spending, you’re also contracting your business, and the revenue will follow, as will employee morale and output.

And if you aren’t yet using law firm accounting software, you’re just planning your law firm’s future based on guesswork. That wouldn’t pass muster for your clients, and it shouldn’t pass muster for your shareholders, either.

The key is to study profitability by timekeeper. This way, you can discern which attorneys are in the clear and which need help. To get the full picture of expenses and profits for every timekeeper, you need to monitor direct expenses, indirect expenses, plus overhead. But most law firm billing platforms can’t deliver this information without running reports from hundreds of general ledger accounts.

Centerbase is here to fill the gap. Our new Profitability Reporting tool delivers the data that your partners need to drive smarter business decisions. Our tool goes beyond showing more than just data on what’s been billed and collected. Our platform helps you track revenue, expenses, and profit margins at the firm, practice group, and individual levels, so you can optimize your firm’s profitability and improve its financial performance. You can also analyze key metrics such as billable hours and realization rates so you can set profitable billing rates and pricing and create accurate budgets. With our platform, you can determine which timekeepers are most valuable to your firm, what practice areas to expand, and which matters are contributing to — and hurting — your bottom line.

Centerbase puts real-time accounting tools in the hands of everyone in your law firm. It’s like having your own personal accountant on call. Contact us for a free demo and learn how our profitability reporting can help you kick-start your law firm’s growth.

Forecasting isn’t only for your local weatherman—it’s an essential legal process too. Fortunately, forecasting income and expenses isn’t as complex as predicting where the next hurricane will hit or when the first freeze of the year will occur. But, when you’re juggling all the tasks of running a law firm, the forecasting and budgeting process can seem both challenging and overwhelming.

Law school courses don’t teach you the practical aspects of running a business, even though they come up every day in real-life practice at a small firm, especially for solo practitioners.

Creating a solid budget and getting your law firm’s finances in order are imperative. This is the only way to stay competitive in the legal market.

The good news is that with the right strategy and management tools, your firm will be off and running. Let’s take a look at these critical processes and what steps you can take to create a budgeting plan.

A budget is an estimate of revenue and expenditures for a specific time period. Basically, it’s your law firm’s plan for sustainable financial success, and budgeting is the process of creating that plan.

Budgeting provides your law firm with a measuring stick for periodic review throughout the next year. If your law firm is hitting its goals, maybe it’s time for an office party! If it’s missing your desired milestones, it’s probably time to re-evaluate and adjust. Creating a comprehensive budget is the best way to proactively manage your law firm’s finances.

A good budget is thoughtful and aligns anticipated revenue and expenses with goals.

What to include in your law firm budget will depend on the size of your firm, how long it’s been in operation, and what practice areas it specializes in. However, there are a few constants for all practices that you should consider when drafting your firm’s budget. Ask yourself these questions.

Don’t start your budget planning in a vacuum. Instead, start by thinking about your firm’s mandatory expenses.

· What is required of the legal professionals at your firm?

· What is the cost of bar association dues?

· What do their CLE expenses look like for the year?

· Does your firm maintain malpractice insurance?

· What is the yearly premium?

· What about subscriptions?

Additionally, think about staffing. If firm leadership is planning to add more employees to the firm, you’ll need to know whether your firm will have money to cash flow that addition. You’ll also want to consider the tangibles: the cost of office space, hardware, and legal and accounting software. What about upgrading to new technology? Or the cost of business cards? Note that some of these expenses will be incurred yearly, some monthly, and some only once.

Once expenses and other overhead costs have been itemized, your next step is to consider profitability (and to do so realistically).

Revenue is the money your firm receives from clients for legal services rendered. When you subtract expenses and overhead costs from revenue, you have net profit (otherwise known as the bottom line).

Think about net profitability in real terms: how many clients will your firm need to service over the next quarter (the next two quarters? the next year?) to bring in the desired level of revenue? Are your firm’s rates high enough to support the practice? What is the required cash flow to keep the lights on? Can improving your invoicing practices improve that cash flow? What about accepting alternative payment methods like credit cards?

If your law firm is hitting revenue milestones without increasing net profit, it means you might need to cut expenses and overhead costs. Be sure to consider seasonality when it comes to revenue. If you’re a tax firm, you’re likely booming in April and slow in July. With awareness, your firm can account for these patterns and set aside capital accordingly so that the necessary funds are still available during less profitable months.

Keeping track of your law firm budget can be time-consuming and stressful. Many new law firms will opt for Excel spreadsheets or budgeting templates to get started with tracking planned expenses and revenue. However, when your law firm grows and its workflow increases, keeping track of your law office budget on those tools might prove even more time-consuming and stressful. The right legal reporting software puts a host of budgeting and financial reports at your fingertips, each of which will help your law firm organize your finances, optimize your practice, and help you strengthen client relationships.

When it comes to how often to review your budgeting process, we recommend assessing your budget each month. This regularity will provide your law firm with a good idea of whether you need to make any adjustments. Additionally, your firm should review its budget yearly to adjust for goals, new practice areas, or unforeseen circumstances (like a market crash or, say, a global pandemic).

While budgeting will look different for each firm, we suggest a couple of tools of the trade to get you started on creating or rethinking your law firm budget.

Setting your law firm goals is one of the first steps in creating a workable budget. Goals are a benchmark to help you determine where to put capital and where to cut costs.

We recommend classifying your goals into the following categories: (1) short-term goals that you can reach in the first six months of your fiscal year, (2) mid-term goals that can be reached by the end of your fiscal year, and (3) long-term goals that will take your firm longer than a year to reach. Also make sure that each set of goals is specifically laid out, measurable, and realistic.

Using the right tools and legal tech can transform a firm’s profitability and law practice management. While it may seem like just another line item expense, technology can actually help keep your costs low through workflow and document automation, which frees up your lawyers and staff to work on billable matters (i.e., tasks that pay).

The right legal tech will help your firm simplify nonbillable tasks like client intake, practice management, billing and collections, and time tracking. With more time for billable work, your firm can raise its revenues. And with the right tech that offers a streamlined experience and integrations, your firm will minimize its use of subscription services and administrative time and thus minimize your overhead costs. The result is the perfect recipe for increased profitability.

We aren’t yet out of uncertain times, and keeping a pulse on what’s to come is important when setting your budget. If your law firm hasn’t yet undergone a full return to the office, your budget may need to include capital for the transition. Or, if your law firm has stayed committed to a hybrid workplace, you might still need to budget for increased tech costs and stipends to employees.

Additionally, many law firms are amplifying their marketing strategies. It’s likely worthwhile to consider how marketing efforts can fit into your budget and increase awareness and thus revenue.

Budgeting and forecasting are both helpful tools that your law firm can and should use to establish a financial plan. As discussed throughout this article, budgeting is the game plan for where firm management wants to take the firm.

Essentially, your budget is an outline of financial expectations and goals. Forecasting, on the other hand, is interpreting whether that plan is working and whether the firm is moving in the right direction by estimating revenue, costs, and ultimately profit that will be achieved at a future date. Generally, forecasting looks at historical data (like last year’s or last quarter’s profits) and then anticipates future outcomes based on it. It’s like a crystal ball, but only better because it’s filled with cash.

Forecasting helps firm management make needed adjustments in practice areas by hiring in anticipation of a boom and, more generally, helps you develop an informed business plan. You can then take that informed business plan into consideration when developing a budget.

With some critical thinking and the right tools, your firm will be ready for the coming year. Remember that no budget is perfect, but by having one in place and monitoring it regularly, your law firm can forecast big changes and adjust as needed.

Think faucet, not ocean. When you think about your law firm’s cash flow, it shouldn’t ebb and flow like the tide. It should be a constant, steady stream.

But if your law firm is like many others, you may have been struggling to ensure your cash flow stays consistent — especially in the aftermath of the pandemic. This can really hurt your firm’s bottom line.

Most small law firms and midsize law firms have past due accounts, which can kill your cash flow and make it possible to pay your employees and bills. And it’s often uncomfortable to ask your clients for money!

Some practice areas may be doing better than others. But no matter the current state of your law practice’s financial health, you’ll always find that there are opportunities to reduce costs, improve lawyer productivity, and get more cash in the door.

If you’re struggling to keep your firm’s cash flow consistent, here are 10 steps that you can take to improve your law firm’s current cash flow.

If you haven’t yet taken the time to do a deep dive into the status of your law firm’s finances, start there. One place to start is by projecting your firm’s cash flow by month, quarter, and year.

Begin by understanding your fixed expenses, such as your rent and utilities. Then add in fluctuating costs such as payroll. Consider whether there are any opportunities to reduce your costs by negotiating with your service providers, such as your phone or internet companies, or to set up a fixed payment structure for your utilities so you can better predict your expenses.

Once you’ve pinned down your costs, it’s time to estimate how much client revenue you expect to receive. This will give you a sense of whether you’ve got a negative or positive cash flow.

Once you get a handle on your law firm’s current finances, you’ll be able to create an accurate cash flow forecast. And with the right practice management software, you’ll be able to quickly generate billing and accounting reports so you can understand your incoming receivables, study where you’re making and losing money, and compare your firm’s cash flow over time.

When legal professionals are busy and stressed, they’re less likely to focus on keeping accurate accounts of where they spend all of their billable hours. If the lawyers in your firm aren’t keeping up to date with the hours they bill, you’re likely suffering from billing leakage. They may be losing up to 30% of their billable time!

This is especially true if you’re working on fixed-fee projects. It’s all too easy for projects to creep in scope and for lawyers to provide work that they don’t charge their clients for. To make it easier for your lawyers to capture every billable minute, implement technology that automatically captures their time throughout the day for calls, texts, emails, appointments, and more.

If you’re struggling to get your clients to pay on time, it may be because there’s friction in your payment processes. Set up a system that accepts different payment options, including online payments, to streamline your invoicing and collection processes. If you aren’t already sending your clients bills by email, now is the time to start.

Typically, accepting credit cards will expedite your payment cycle and make it easier to track incoming cash. It may be worth paying a small convenience fee to a processor to get payments in the door more quickly.

Speeding up payment requires firms to lower the time between completion of work and billing. Make sure your lawyers are invoicing for their billable hours as soon as possible — either when work is completed or at a reasonable point in the interim.

If your attorneys take too long to review their bills, send them reminders and set a policy that bills must be reviewed within a set number of days. Clients don’t like it when they receive bills months after work is completed. And it’s often helpful for clients to receive a bill at the beginning of the month, which is often right after their payday.

You may also entice clients to pay faster if you offer a discount for earlier payment, such as within 15 or 30 days of your invoice. Typical discounts are between 3 and 5 percent of the bill.

The longer an invoice remains open, the less likely it is to be paid, so review your accounts receivable regularly and set a cadence for following up.

It can be uncomfortable to ask clients for payments. But it’s necessary to have these conversations and offer your clients a solution, if necessary. Instead of asking clients when they can pay you and how much, it’s often more effective to present payment plans to your clients. Consider proposing a 60-day plan with installment payments, which may make the overdue amount more palatable. Another effective strategy is offering clients a brief email reminder with a link to pay online.

Because lawyers in your firm may worry about jeopardizing client relationships, it may make sense to have a billing or accounting professional manage the collections process; you may also want to consider outsourcing collections to a third-party provider.

If your client retainers are running low, increase them before you run out to avoid shelling out cash that won’t be replenished immediately.

You should also avoid surprising clients with billing for items they don’t expect. Make sure your agreements spell out upfront what new clients should anticipate. If you have an unexpected expense or if you have a large bill, prepare the client with a short call to make sure they fully understand the cost before they get your invoice. This way, you’re more likely to avoid the need for write-offs.

Make sure that you are paying your bills when they’re due. If you pay them after their due dates, you’re likely exposing your firm to late fees. And if you pay too early, you’re tying up cash that you could use for other purposes.

You should have enough cash saved up to cover all of your law firm’s expenses in case of a rainy day (or, say, a global pandemic). Use your cash flow analysis to predict your expenses and set aside an amount sufficient to pay your firm’s bills for three months. That way, you won’t have to panic in case you experience a seasonal slump or another temporary downturn.

Some law firms also establish a line of credit to ensure they have an additional financial cushion in the event of a shortfall. If you don’t use it, you won’t incur any interest, and it will be there for you when, and if, your firm needs it.

Setting reasonable key performance indicators will help you keep your firm on the right path. For example, you might track the number of days that bills remain outstanding and measure whether that number drops over time. Or you might study the change in your working capital over time, which is a ratio of your current assets divided by your current liabilities.

You can also account for variances that may account for any changes in your forecasts. The possibilities are almost limitless, especially if you have access to reporting features in your billing or practice management platform.

The most successful law firms integrate their accounting processes with a cloud-based practice management software platform that helps them improve their firm’s efficiency, productivity, and profitability.

When your firm chooses the right technology, you help your timekeepers eliminate countless minutes that they would otherwise spend on administrative tasks — including timekeeping, invoicing, and collecting on overdue invoices — that take away from your revenue. And you can more accurately (and quickly) project your firm’s finances and study your historical and projected cash flow so you can plan more accurately and set realistic goals for the months and years to come.

We’ve talked before about the importance of legal analytics and legal technology for law firms. If you’ve already made the leap to using a cloud-based legal management system, you might be overwhelmed by all the data it’s collecting. After all, most lawyers don’t moonlight as statisticians.

It’s difficult for leaders to know what metrics are the most important for the firm’s success in the long term and how to use those metrics to make higher-level decisions that help drive law firm profitability. The best way to start is by tracking the metrics with a convenient and easy-to-use tool that keeps them organized all in one place.

That tool is called a dashboard. Every law practice can use dashboards to easily track financial metrics, make informed decisions, and grow their business.

A dashboard is a customizable page that uses simple graphs and visuals to monitor key performance indicators (KPIs) in real-time.

Usually, a dashboard is a landing page and part of a larger cloud-based law firm management platform. Dashboards provide law firm management with an easy-to-digest snapshot of the metrics and relevant data for their goals. Instead of struggling to understand the big picture, dashboards provide much-needed perspective and turn raw data into actionable information.

Dashboards are a tool to help law firms increase productivity and stay on track. They empower law practice management to monitor progress and make informed decisions that drive firm strategy, hiring, staffing, pricing, and more.

Dashboards aren’t just for law firm management. They can also help lawyers and staff monitor appointments, tasks, and individual metrics. Access to dashboards helps employees stay on task and improve their collaboration while allowing management to do a deeper dive into individual employee productivity.

Data points are raw numbers without any context. Data points are the building blocks for the information that is displayed on the dashboard. Data informs metrics and KPIs and the graphics that appear on your screen.

Legal technology platforms constantly collect data. For example, when timekeepers input data (like their billable hours or completed tasks) into a case management system, it is automatically populated and incorporated into other aspects of the software and may also interface with other technology solutions.

A great example of a data point is the number of employees in your law firm, the number of daily website views, or an employee’s time spent on a particular task, like billing. Data points are different from metrics because you can’t influence them. Data is data, no matter how you spin it.

Metrics add meaning and context to data sources and inform KPIs. Metrics measure the overall health of a law firm. Law firms track key metrics to create KPIs that measure progress toward achieving a larger business goal.

Some examples of metrics are the actual minutes or hours that lawyers spend on particular billable tasks per week (instead of just a raw number), the lawyer turnover rate in the office, or the percentage of new clients who view the website and request a consultation.

KPIs reflect a law firm’s progress (or lack of progress) toward achieving a particular goal. They are forward-thinking data collected to analyze productivity.

KPIs are based on specific metrics related to different aspects of a law firm’s functionality, including budgeting and billing, education and training, overall client satisfaction, and internal processes. The law firm’s leaders identify a goal based on the metrics and then use KPIs to measure progress toward that goal.

KPIs based on our example above include reducing the time that lawyers spend on billing processes by 25% each month, generating 30% more clients in the upcoming year, or retaining employees for at least 3 years.

Data points are the foundation for a metric, which gives data meaning. Then the metric (or multiple metrics) are used to create a KPI and monitor progress towards a particular goal.

Dashboards are only as helpful as the information that they display. Even though they are simple, dashboards require some forethought to set up. Legal practice leaders should take time to customize their dashboards to be the most practical and effective.

Before using your dashboard, you’ll need to have KPIs. A clearly defined KPI helps you achieve your business goals. It keeps everyone in the office on the same page and makes your dashboard more useful. A well-defined KPI is SMART: it is specific, measurable, attainable, realistic, and time-bound, meaning that it has a specific deadline.

A great example of a KPI is to bill 25% more hours in the first half of the fiscal year. This KPI is clearly defined so that every timekeeper can get on the same page. It is a realistic goal that can be measured and tracked throughout the designated period.

A dashboard is designed to be a snippet overview of your progress toward reaching KPIs and the health of your law firm. Most law firms have many different business goals that change over time. It is important that you declutter your dashboard and only focus on the most important KPIs for your purposes.

If there is too much information on your dashboard, it takes away from the tool’s simplicity. The more data that’s displayed, the harder it is to quickly digest important trends and track progress. As time passes and you reach certain goals, you can re-evaluate your dashboard and add or subtract KPIs as necessary.

The great thing about dashboards is that you can have more than one. Instead of having a dashboard that tracks everything under the sun, you can set up different dashboards for each area of the business. For example, you should have a dashboard dedicated to financial metrics and a separate one dedicated to client metrics.

Using multiple dashboards also lets employees track the metrics as they relate to their own performance and responsibilities. To reach your law firm goals, you’ll need to rely on your staff. By giving timekeepers access to their own dashboard and the ability to track their own metrics, it keeps them focused and sets clear expectations for their work. Instead of nagging lawyers about how they spend their time, they can self-monitor and make adjustments along the way.

Your law practice can use a legal dashboard to track just about any metric. Law firms should consistently track financial, learning and growth, client services, and project management metrics for every practice area. Each of these categories should have a dashboard that reflects the KPIs related to them.

Of course, many of these metrics tend to relate to a law firm’s financials. After all, streamlining internal processes, increasing lawyer productivity, and having happy clients all affect revenue. An easy way to start is by creating a dashboard to track financial metrics.

Small and mid-size law firms that want to grow will benefit from tracking some combination of the following financial metrics:

Just because law firms should track all of these financial metrics doesn’t necessarily mean they should all be included on the same dashboard. Law firms need to take the time to identify the metrics that are specific to reaching their financial KPIs. Law firm management may opt to have multiple financial dashboards that subdivide these metrics even further.

A well-thought-out dashboard can benefit a law firm by driving productivity and helping the overall business development. Dashboards help law firm leaders turn data into usable information to inform decision-making. They are an excellent tool to track financial performance and monitor the firm’s finances without wasting time staring at meaningless numbers. Dashboards can also be used in conjunction with other best practices, like reporting, to increase the bottom line.

Well-organized dashboards can also keep law firm management focused on the big-picture goals for the business instead of getting bogged down in the minutiae. Plus, dashboards can help keep everyone in the office on the same page about firm performance and give them the business intelligence they need to focus on their role in growing the firm.