Annual planning is an essential exercise that can help you position your law firm for long-term success. It also helps you adapt to external challenges like regulatory changes, evolving client expectations, and heightened competition. Annual planning provides:

Clear direction: A well-defined roadmap aligns your firm’s objectives with actionable steps.

Proactive strategy: You’ll ensure resilience by anticipating challenges and leveraging opportunities.

Enhanced decision-making: A structured, data-centric approach to allocating resources efficiently and setting achievable goals lessens the stress of making decisions.

It can be a daunting process, but in this article, we’ll offer a practical approach that focuses on profitability analysis.

Conducting annual planning through a lens of profitability ensures you go beyond the simple calculation of Revenue – Expenses = Profitability to incorporate multiple components that feed into profitability. These include operational efficiency, cost structures and billable rates, revenue optimization, cost management, attorney career paths, and strategic technology usage.

This constructive planning method, based on key insights from our Annual Planning Guide for Law Firms, offers insights to align your law firm’s objectives with actionable strategies that achieve increased efficiency and create a foundation for sustainable growth.

Understanding & Conducting Law Firm Profitability Analysis

Understanding profitability is a fundamental step in the annual planning process, serving as the foundation for strategic decisions and resource allocation. By identifying key metrics and operational inefficiencies, you can begin to develop a roadmap for enhanced growth and efficiency.

Profitability in law firms extends beyond simple revenue calculations. A deep dive into operational metrics reveals opportunities for optimization:

Lawyer Cost Structure and Billable Rates: Calculate the cost rate for each attorney by including salary, benefits, office space, and technology expenses. For example, an attorney with a $120,000 annual salary, 100 billable hours per month and $100 per hour in overhead costs must bill at least $200 per hour to break even.

Practice Area Profitability: Identify which practice areas generate the most profit by comparing revenue to associated costs. Look at attorney utilization rates within each area, too. Are higher-cost attorneys working on lower-value matters? Reassign that work to lower-cost attorneys to improve practice area profitability.

Client Profitability: Track the time spent and revenue generated per client. Focus on high-value clients and renegotiate terms, or shift focus away from resource-intensive, low-value relationships.

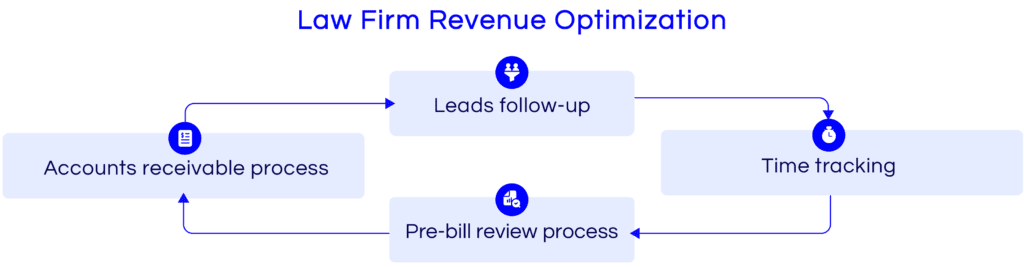

Revenue Optimization: Optimize revenue generation by following up on leads consistently, capturing all billable time, minimizing write-offs, and optimizing accounts receivable collections. Make sure you have processes, policies, and tools in place to enable these optimizations.

Aligning Equity and Compensation with Growth

As firms refine their profitability strategies, aligning equity and compensation becomes a logical next step to ensure that financial incentives drive behaviors consistent with the firm’s goals.

Compensation structures play a pivotal role in driving profitability. Consider these strategies:

Business Development Incentives: Reward attorneys who expand client relationships or bring in new business.

Value-Based Compensation: Align pay structures with firm values, including non-billable contributions like mentoring and leadership.

Transparent Career Pathways: Define clear criteria for partnership advancement, ensuring alignment with both financial goals and firm culture.

Leveraging Technology for Profitability

Technology is a critical enabler of efficiency and profitability in law firms and should be viewed as a revenue multiplier. During your annual planning process, evaluate your tech stack. Are your current tools being fully utilized? You should be leveraging technology to improve profitability through key capabilities, including:

Adopting Comprehensive Solutions: Use integrated platforms like Centerbase, which combine matter management, billing, timekeeping, and CRM in one system.

Streamlining Processes: Automate time capture, lead management, and billing workflows to reduce manual errors and save time.

Investing in Training: Provide ongoing education to ensure staff can fully leverage existing tools.

By aligning technology with firm objectives, you can enhance client experiences, reduce inefficiencies, and stay competitive.

Developing a Strategic Growth Plan

The topic of growth inevitably will be part of your annual planning discussions. Remember, growth doesn’t have to be just about increasing headcount. A strategic approach to growth focuses on increasing efficiency and profitability, and deepening client relationships.

Consider incorporating these components into your growth plan:

Optimizing Marketing: Use data-driven marketing strategies to attract the right clients to your firm. These clients are best aligned with your firm’s strengths and capabilities, ensuring your ability to deliver the results they need.

Optimizing Attorney Career Paths: Provide mentorship and define expectations at every career stage, from associate to equity partner, to enhance retention, productivity and ultimately profitability.

Strengthening Client Relationships: Cross-selling can be a multiplier for nearly every firm, so leverage these opportunities to maximize value from existing clients. Try to do everything you can for the clients already coming through your door.

Enhancing Efficiency: Streamline workflows to improve operational effectiveness without overburdening resources.

Implementing and Sustaining the Plan

Annual planning, driven by a focus on profitability, equips law firms with the tools to navigate industry challenges and achieve strategic goals. By aligning resources, leveraging technology, and fostering a culture of continuous improvement, you can position your firm for lasting success.

Your key actions to implement and sustain a successful plan include:

Assign Roles: Define clear responsibilities to maintain momentum.

Foster a Culture of Improvement: Encourage regular reviews and training to adapt to evolving needs.

Monitor Progress: Use key metrics to track performance and adjust as needed.

For more insights and tools to streamline your law firm’s operations, explore Centerbase’s solutions.

Family law firms face unique challenges that require innovative strategies to ensure long-term success. In advance of the AAML Annual Meeting in Chicago, Affinity Consulting Group, Centerbase, and 12 AAML fellows discussed how family law practices can adapt to future demands.

The conversation centered around three critical areas: profitability, the transformative role of AI in family law, and cultivating a strong, people-centered firm culture. This summary captures the group’s insights and actionable recommendations, offering a roadmap for family law firms looking to thrive in a competitive and tech-driven future.

Focus on Profitability to Maximize Resources

Profitability is an important measure of success for any law firm because it helps determine how efficiently the firm utilizes resources and how much value it delivers to clients. Measuring law firm profitability requires analyzing the underlying factors that influence profitability’s core components — revenue and expenses — which helps you identify opportunities to maximize profits and make data-driven decisions.

Actions to Take

Enhance Collection Processes: Create or strengthen a collections team to handle outstanding payments, minimizing the need for attorneys to follow up with clients. Use tools to automate alerts for retainer replenishments and overdue accounts.

Implement Clear Payment Policies: Develop a standardized approach that informs clients upfront about retainer requirements and account replenishments.

Introduce KPIs: What gets measured gets done, so establish collection goals (e.g., 90%+ collection rate) to improve financial predictability and accountability.

Leverage Technology: Consider software that offers automated time capture and billing to reduce lost hours. Tools such as Laurel AI or Centerbase’s Automatic Time Capture can help track all billable activities.

Use AI for Good in Family Law Practice

The usage of AI is changing the way attorneys and law firms operate for good. But rather than fearing AI, the mindful adoption of AI offers tremendous promise to enhance the way legal professionals work, reducing tedium in the practice of law while freeing up valuable time for thinking strategically, identifying creative solutions, and engaging thoughtfully with clients. Embracing AI thoughtfully is an act of helping your firm operate in a modern legal landscape.

Actions to Take

Explore Recruiting AI: Use AI-driven tools to scrape platforms like LinkedIn, identifying and compiling lists of qualified candidates without relying on costly recruiting agencies.

Automate Document Review: Use AI tools like Paxton.ai and Co-Counsel to handle initial drafts of discovery summaries, deposition reviews, and document comparisons.

Improve Written Communication: Grammarly and WordRake are tools that can improve clarity and professionalism in client communications.

Make AI Your Thought Partner: Utilize ChatGPT for brainstorming, drafting, and researching by posing prompts such as, “Suggest 5 innovative growth strategies for a family law firm.”

Integrate Time Capture AI: Investigate AI solutions to improve billing accuracy by capturing all activity data throughout the day. This helps avoid revenue loss from unbilled hours.

Foster a Culture that Values Your Firm’s People

Your people are your number one asset. Prioritize onboarding and retention strategies that help you take care of your team and build a strong culture centered on the firm’s values. Implementing these strategies proactively will help safeguard against costly employee turnover and set your firm up for greater success.

Actions to Take

Clarify and Communicate Core Values: Define core values and communicate them regularly across the team.

Onboarding and Training Programs: Build structured onboarding programs for associates, setting clear expectations, goals, and values from day one. Consider implementing a “University” program, where experienced attorneys mentor newcomers and provide training in core legal and business skills.

Host Regular Team Check-Ins: Hold weekly meetings to discuss progress, address challenges, reinforce cultural values, and provide feedback for associates’ development.

Create a Knowledge Library: Develop a knowledge-sharing system with standardized documents and training videos so team members can access firm-specific procedures and templates.

Encourage Peer Learning and Mentorship: Foster an environment where senior attorneys regularly provide feedback and mentorship, enhancing skills and strengthening relationships within the firm.

Embrace Progress to Build Your Firm’s Future

Family law firms have an opportunity to set new standards in how they serve clients, support their teams, and use technology to streamline their operations. Embracing this future requires a commitment to rethinking traditional approaches to profitability, talent management, and the role of AI. Now is the time to assess your firm’s strengths and identify where these strategies can make a meaningful impact.

Law firm profitability is often viewed in simplistic terms: the more billable hours attorneys log, the more profitable the firm becomes. But the reality of assessing profitability is far more nuanced. Profitability can be sliced and diced in several ways — by practice area, client, lawyer, and matter profitability, and more — and your firm has to determine what’s appropriate to analyze.

That can get complicated, but my goal with this article is to help make profitability analysis feel doable by looking at just one example — practice area profitability. We’ll look at how you can use practice area information to make strategic decisions about resource allocation, maximizing your profit margins, and maintaining a healthy work environment for your attorneys and staff.

Understand Attorney Cost Rates to Set a Profitability Foundation

Before we can begin analyzing profitability by practice area, we must understand what it costs your firm to provide its services by determining each attorney’s cost rate.

This is essentially the hourly cost of employing them, including salary, benefits, and overhead expenses such as office space and technology. This rate forms the foundation for assessing whether your firm is pricing its services appropriately and whether each attorney is contributing to overall profitability.

Base salary and benefits: The most straightforward cost is the attorney's salary, along with additional benefits like health insurance and retirement contributions.

Overhead allocation: Overhead includes office space, administrative support, technology costs, and other general expenses. Allocating these expenses to each attorney is essential for a true understanding of their cost.

Practice group specifics: Different practice groups may require varying levels of support or incur different costs. For example, a litigation group may need additional paralegal support compared to a transactional group, affecting the cost rate of attorneys in that practice area.

Calculate the cost rate for each attorney by adding their salary and benefits to their share of overhead expenses. This will give you a baseline cost per hour for each attorney, which can then be compared to their billing rate to determine their contribution to profitability.

Practice Area Profitability: Analyzing Where the Firm Thrives

Now that you’ve established attorney cost rates, you're ready to analyze profitability by practice area. This is often a relevant category to assess within a firm because it can reveal valuable insights that might not be apparent from a high-level overview of your firm's financials.

For example, a firm may appear profitable overall but harbor unprofitable practice areas that are being subsidized by more successful ones. This situation can lead to resentment among partners and potentially affect staff retention.

Not all practice areas are created equal — some may generate substantial revenue but come with high costs, while others may be highly efficient profit centers.

You can understand practice area profitability at both a high level and a granular level. By breaking down profitability by practice area, firms can identify which areas are driving the most profit and which may be underperforming. Here are some guidelines to approach this analysis:

Revenue vs. costs: Start by calculating the total revenue generated by each practice area. Then, subtract the costs associated with that practice area, including attorney cost rates, paralegal support, and other direct expenses. This will give you a clearer picture of each practice area’s profitability.

Attorney utilization: Consider the utilization rates of attorneys within each practice area. Are higher-cost attorneys working on lower-value matters? If so, reassigning that work to lower-cost associates could improve profitability.

Market rates and adjustments: The cost rate analysis also helps determine if the billing rates for specific practice areas are appropriate. If a practice area isn’t profitable, you can explore adjusting the rates or targeting different types of clients.

You want to regularly assess the profitability of each practice area by tracking revenue, costs, and utilization rates. Adjust resource allocation to ensure the right attorneys are working on the right matters to maximize profitability.

Leverage and the Concept of 'Highest and Best Use'

Another crucial factor that impacts profitability is how work is allocated across the firm. The concept of “highest and best use” can help ensure that the right person is doing the right work at the right time. This is particularly important for maximizing profitability in practice areas with mixed levels of complexity.

Partner vs. associate work: Partners typically have higher billing rates but also higher cost rates. Ensuring that partners focus on strategic, high-value tasks while associates handle routine work can help improve profit margins. The key is to avoid having high-cost attorneys working on tasks that can be done just as effectively by lower-cost attorneys.

Utilizing technology and support staff: Law firms should also leverage technology and support staff to handle tasks that don’t require an attorney’s expertise. Choose law practice management software for time tracking, document management, and other administrative functions to reduce the amount of time attorneys spend on non-billable activities to further enhance profitability.

Conduct regular reviews of workload distribution to ensure that partners, associates, and support staff are all working at their highest and best use. This will help optimize profitability while maintaining a balanced workload across the firm.

Benchmarking and Profitability Tracking

Benchmarking plays an important role in understanding whether your firm is performing as well as it should be. You can benchmark against both internal and external standards to identify areas for improvement and set realistic goals for growth.

Internal benchmarking: Compare the profitability of different practice areas, clients, and attorneys within your firm. Identify which areas are excelling and which need improvement. Then, use these insights to guide strategic decisions.

External benchmarking: Look at industry benchmarks for profitability, revenue per attorney, and other key performance indicators. This will help you understand where your firm stands compared to your peers and identify opportunities to enhance profitability.

Use benchmarking data to set performance targets for practice areas and individual attorneys. This will help create accountability and ensure that everyone in the firm is aligned with profitability goals.

Turn Insights into Action

Maximizing profitability requires moving beyond increasing billable hours to taking a holistic approach. This should include understanding attorney cost rates first, and then analyzing a category that makes sense for your firm, such as practice area performance. With this combined cost rate at practice area data, you can begin allocating resources strategically — all to identify hidden opportunities for growth, make data-driven decisions, and ensure long-term profitability for the firm.

By Paige Roncke, Chief Revenue Officer, Centerbase

The legal industry is at a critical inflection point where law firms can no longer identify only as legal services providers. Law firms must also be data and technology companies in order to effectively compete in the market for long-term success.

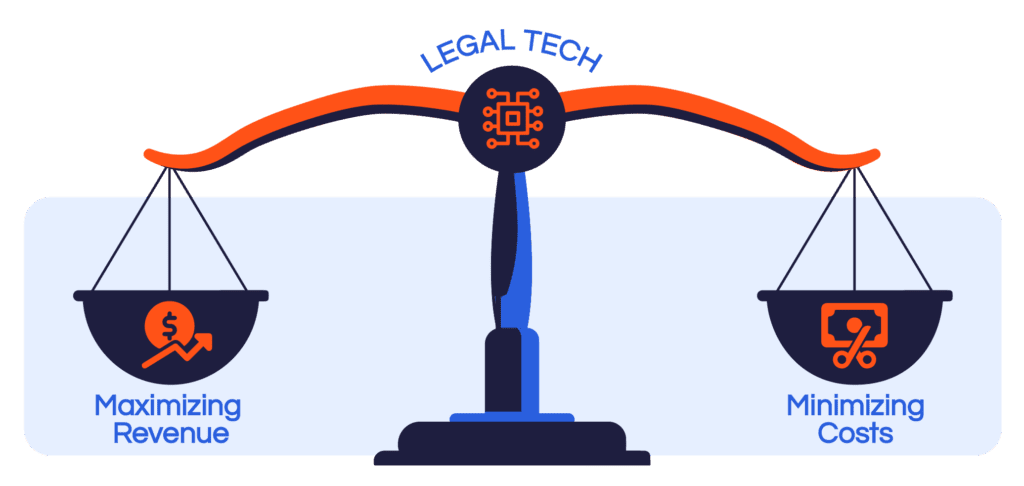

I discussed this new landscape with Debbie Foster, CEO of Affinity Consulting, during a webinar on law firm profitability. A substantial portion of that conversation was rooted in the theory that profitability is more than a simple math formula of revenue minus cost; rather, it’s about understanding your firm's opportunity to maximize revenue streams while also minimizing costs without compromising quality of legal services.

It’s a misnomer to assume the application of technology only minimizes cost. Yes, technology has a critical role in automating administrative tasks, optimizing billing processes and creating comprehensive and speedy communications both internally and externally. However, technology is best utilized when the full power of software is applied to maximizing potential revenue streams.

This can be software-driven enhancements like improving time capture to create more billable hours, building reports that provide deeper insights into profitability at various levels — from individual attorneys to entire practice areas — through data clarity and availability, and utilizing that data to retain and attract stronger talent that can bill at higher rates.

In other words, as Debbie stated, “Technology should be used as a revenue multiplier.” And multiplied revenue leads to greater profitability.

While many firms have already made investments in technology, they may not be fully utilizing these tools. Let’s examine how technology can enhance law firm profitability by improving time tracking, managing billing, and providing actionable insights into the firm’s financial health. We'll also discuss common technology pitfalls and how to avoid them, so your firm can make the most of your technology investments.

Where Technology Drives Profitability in Law Firms

With the right tools, firms can unlock efficiencies that translate directly into higher profits. The key is knowing how to leverage technology effectively to improve law firm profitability, such as:

Improve timekeeping: It’s no secret that lawyers often fail to capture all of their time, which represents a direct loss of revenue. Automatic time capture technology can ensure that all billable hours are accounted for, leading to increased revenue. Text messages, quick phone calls, emails, a few minutes spent editing a document — all those moments add up to billed time. Time tracking software will track it all, automatically.

Enhance collaboration: Cloud-based technology makes it easier for attorneys and staff to collaborate, share documents, and manage cases from anywhere. It also provides access to real-time data and communication tools, enabling better decision-making and faster responses to clients, which ultimately improves client satisfaction and retention.

Streamline billing and reduce write-offs: Legal billing software can automate the entire invoicing process, from generating accurate invoices based on captured time to sending automated payment reminders. As a result, you’ll invoice faster and more accurately, reducing write-offs and improving cash flow.

Optimize resource allocation: How effectively does your firm analyze profitability by practice area, client, and individual lawyers? Practice management systems track all aspects of a case, from time spent to expenses incurred. The system will then generate profitability reports that reveal profitability across multiple dimensions. You can use the data to allocate resources more effectively, ensuring that the most cost-effective lawyers do the most profitable work. You can also use this data to make investment decisions when determining which practice areas to fund or reallocate.

Improve collections: Tools like online payment portals and automated payment reminders can automate and streamline the collections process, reducing the amount of time it takes to collect outstanding invoices.

Streamline lead management: On the marketing side of running a law firm, technology can help you respond to leads quickly and efficiently, improving your chances of converting them into paying clients. This could involve using tools like customer relationship management (CRM) software, live chat on your law firm's website, and streamlined client intake workflows.

Promote a culture of continuous improvement: Fostering a culture where employees are encouraged to learn and use new technology can help you stay ahead of the curve and maximize your firm’s technology investments.

Technology Shouldn’t Be the First Budget Reduction

Despite these opportunities to use technology as a revenue multiplier to drive significant profitability gains, many firms struggle to fully leverage the tools they have — and that often leads to cutting technology costs. But cutting costs isn’t a sustainable path to profitability.

Consider these common pitfalls to avoid so you can maximize your technology to advance your revenue streams.

1. Underutilizing Software Features

Many law firms invest in technology but only use a small fraction of the available features. For example, your firm might not be taking full advantage of your practice management software’s time tracking, billing, and reporting features that could improve efficiency. Leveraging a tool’s full capabilities can not only improve efficiency but help reduce stress at work, too. Encourage continuous learning, where attorneys and staff explore new features and share tips for improving efficiency.

2. Lack of Ongoing Training and Support

Too often, technology implementation is treated as a one-time event rather than an ongoing process. A lot of effort goes into the rollout and not enough into continuous training to learn about the tool after it’s been implemented.

As Debbie says:

“We really need to marry up our technology spend with building a culture of training.”

Pay attention to new updates and features, and make sure your staff learns how to use them by providing ongoing training and support. Consider hosting monthly lunch-and-learn sessions to discuss new ways to use your tools more effectively.

3. Not Using Technology to Attract and Retain Talent

One of the best things technology can do for your firm is standardize processes. Sure, every lawyer prefers to do certain things differently, but technology can help you agree on standardizing core elements of practicing law and running a firm. The result goes beyond efficiency.

New associates coming out of law school want to gain experience with modern technology — and they expect it. Maximizing your technology presents your firm as forward-thinking and committed to providing resources to work effectively, and that can help you stand out as an employer of choice.

Newer technology presents employees with an enhanced user experience with fewer clicks, simpler and more modern interfaces, and intuitive ease of use. This streamlined experience over older systems leads to higher job satisfaction, boosting your talent retention and attraction.

The Future of Law Firm Profitability is Powered by Technology

Technology is no longer optional — it’s essential for creating a long-term competitive edge. Whether it’s automating time tracking, streamlining billing, or analyzing profitability across practice areas, the right tools can make all the difference in how efficiently your firm operates.

By embracing technology and ensuring it is fully integrated into your firm’s processes, you can unlock new levels of profitability, improve client satisfaction, and future-proof your business for years to come. The key is not just investing in technology but leveraging it to its full potential—and continuously improving how you use it through ongoing training and fostering a culture the embraces technology.

Written by Robin Neill

More and more law firms are recognizing how important it is to manage themselves like a business to survive in today’s competitive market. Businesses operate with efficiency, strategic planning, and a keen eye on the bottom line — principles that law firms can adopt to enhance their operational effectiveness. By embracing business management practices such as budgeting, law firms can optimize their resources, streamline processes, and invest in technology to improve their service.

A budget provides a structured roadmap for financial stability, strategic decision-making, and sustainable growth. Creating a law firm budget requires careful planning, collaboration, and attention to detail. Here are seven steps that can help your law firm create an effective budget.

1. Start the budget planning process early

Budgeting shouldn’t be a last-minute task. Law firms should initiate the budgeting process well in advance, ideally in the third quarter. Starting early ensures firms have ample time to assess their current financial standing, analyze past spending patterns, and anticipate future costs.

2. Analyze past performance to project future expenses

A fundamental step in budgeting is examining the firm’s profit and loss (P&L) statement from previous years. By comparing actual expenditures with previous years’ data, law firms can identify trends and patterns.

Areas to focus on include salaries and rent, which tend to be the largest expenses in a law firm budget. Don’t forget to consider inflation.

3. Set clear goals

Setting clear, measurable, and realistic goals is fundamental to the budgeting process — and those goals must align with the firm’s overall strategic objectives. Whether the aim is to sustain current levels of success or to expand to new locations or practices, having a well-defined vision guides the budgeting process effectively.

For instance, a law firm planning to increase its partner count from 10 to 20 in the next year needs to account for higher advertising costs, additional attorney salaries, and potential increases in professional dues and liability insurance.

4. Involve the right stakeholders

Successful budgeting necessitates collaboration between key stakeholders. This includes financial experts, managing partners, human resources professionals, and accountants. Each participant brings a unique perspective to the table, ensuring that the budget addresses all aspects of the firm’s operations.

Regular consultations and brainstorming sessions with these stakeholders can provide invaluable insights and foster a culture of financial transparency within the firm.

5. Consider unforeseen expenses

While analyzing the P&L statement, law firms often overlook certain unexpected costs. Items such as professional liability insurance, litigation expenses, or regulatory compliance costs can fluctuate, impacting the budget unexpectedly. By accounting for these variables and having a contingency fund, firms can avoid financial strain when unforeseen expenses arise.

6. Focus on employee well-being and benefits

Recognizing that employees are a firm’s most valuable asset, law firms should offer a competitive salary and benefits such as health insurance, retirement plans, and professional development opportunities. A comprehensive benefits package can attract top talent and ensure staff retention and satisfaction. Additionally, employee well-being initiatives such as mental health support programs or flexible work arrangements can enhance productivity and foster a positive work environment.

Law firms must factor in the costs of these employee benefits while budgeting. Firms should also take into account salary increases, such as cost-of-living adjustments, to stay competitive in the market.

7. Leverage legal software and other analytical tools

Law firms should invest in advanced legal software with accounting features to track expenditures efficiently. These legal technology tools provide detailed reports on profitability based on various parameters, such as attorney performance, case type, and office location. Implementing artificial intelligence-driven tools can deliver insights into future financial trends and assist firms in making proactive budgeting decisions.

Budget now and your law firm will reap the rewards later

Transforming a law firm into a business entity demands a proactive approach to budgeting. Law firms can use budgets to position themselves for sustainable growth, client satisfaction, and long-term success.

Centerbase has a robust suite of tools designed to optimize law firm financial performance. Get in touch for a free demo of our tools and learn how our software can improve your law firm’s profitability.

Written by Carol Patterson

For five quarters in a row, law firm profitability has fallen, according to the 2023 Report on the State of the Legal Market, a study conducted by the Thomson Reuters Institute and Georgetown. (Data are based on reported results from 170 US-based law firms, including 46 AmLaw 100 firms, 47 AmLaw 200 firms, and 77 midsize law firms.) Profits per equity partner are down for the first time since 2009. Client payments and realization rates are down too.

Demand has also dropped for everyone except midsize firms, where clients are flocking because they want quality legal services without the major firm price tag.

So, how can small and medium-sized law firms capitalize on this demand and optimize their profitability? That’s what we’ll cover in this article.

Why does profitability matter for law firms?

Law firms should focus on profitability for a number of reasons. First, being profitable ensures that the firm can sustain its operations and provide quality legal services to clients. Having a profit allows firms to comfortably cover their operating expenses, such as rent, salaries, technology, research materials, and marketing, and establish contingency funds and reserves for unexpected expenses or downturns in business, such as a global pandemic, potential lawsuit, or market uncertainties.

It’s also important for law firms to have sufficient funds to invest in resources and infrastructure to stay competitive and deliver efficient services. To stay ahead of the curve, firms should make investments in technology, legal research tools, document management systems, communication tools and client portals, matter management systems, and training. The more profitable a firm is, the better it can enhance its capabilities and client service through investments like these. And the more investments a firm makes, the better able it is to attract, engage, and retain attorneys and staff members — not to mention pay them competitively.

Finally, profitable law firms are positioned to pursue growth opportunities and expand their practice areas or geographic reach. They can invest in client and business development strategies that attract new clients and increase their market share.

Why do law firms miss their profitability goals?

The baseline profitability goal for a law firm is 50 percent. If your firm isn’t hitting that mark, it may be because your expenses are too high or you aren’t earning enough revenue. Or maybe you are too heavily staffed, which can drain your law firm’s financial resources. The key is to figure out what is causing the problem.

Many firms look at their profit and loss statements, but these statements don’t tell you the whole story. The typical law firm P&L report isn’t granular enough to help you determine the true source of revenue and expenses. You may have a timekeeper who brings in a lot of revenue but not enough to cover their incredibly high expenses, for example. Or you may have a million-dollar client, but what you shell out to keep that client and maintain their business is so high that you’re essentially paying the client to remain on your roster. But you likely can’t tell that from your current financials.

The problem stems from too many law firms not running their firms like a business. Law firms that lack accountants don’t fully understand the concepts of what makes firms profitable. If your firm’s office manager or paralegals are managing your accounting, they are certainly capable of handling billing, checks, and cash receipts, but they won’t be able to focus on your law firm’s bigger financial picture.

The bottom line is that if you’re focusing just on revenue and expenses, you’re missing important details. Many law firms overreact when expenses look high and look for ways to make cuts. But if you’re focused on reducing spending, you’re also contracting your business, and the revenue will follow, as will employee morale and output.

And if you aren’t yet using law firm accounting software, you’re just planning your law firm’s future based on guesswork. That wouldn’t pass muster for your clients, and it shouldn’t pass muster for your shareholders, either.

What is the best way to monitor law firm profitability?

The key is to study profitability by timekeeper. This way, you can discern which attorneys are in the clear and which need help. To get the full picture of expenses and profits for every timekeeper, you need to monitor direct expenses, indirect expenses, plus overhead. But most law firm billing platforms can’t deliver this information without running reports from hundreds of general ledger accounts.

Centerbase is here to fill the gap. Our new Profitability Reporting tool delivers the data that your partners need to drive smarter business decisions. Our tool goes beyond showing more than just data on what’s been billed and collected. Our platform helps you track revenue, expenses, and profit margins at the firm, practice group, and individual levels, so you can optimize your firm’s profitability and improve its financial performance. You can also analyze key metrics such as billable hours and realization rates so you can set profitable billing rates and pricing and create accurate budgets. With our platform, you can determine which timekeepers are most valuable to your firm, what practice areas to expand, and which matters are contributing to — and hurting — your bottom line.

Centerbase puts real-time accounting tools in the hands of everyone in your law firm. It’s like having your own personal accountant on call. Contact us for a free demo and learn how our profitability reporting can help you kick-start your law firm’s growth.