How to Use Cost Accounting to Determine Profitability

How are changes in today’s climate impacting your law firm profitability? Technology has changed our world significantly, and law firms are slowly catching up to the rest of the business world in many areas. Gone are the days of the large offices, where every attorney has their own secretary, and the firm houses a large library full of books that must be manually updated with those supplements that would arrive on a regular basis, much to our chagrin.

As we have slowly joined the rest of the world in the ways of online research and paperless offices, we are also considering more appropriate ways to look at profitability. This is due, in part, to client demand. Clients no longer accept the idea that they will pay our firms by billable hour, with no budget or foreshadowing of what their final out-of-pocket expense may become. Technology allows for broader communication and stiffer competition, and if we want to remain competitive, we must become more efficient and readily able to consider alternative fee arrangements (AFAs) such as flat fees, risk collar agreements, etc., or at the very least, offer accurate budgets that clients can count on so that they know their worst-case scenario.

While we may have given in to the fact that we must agree to these terms in order to get the work, many firms find themselves no longer profitable as a result. Where they are falling short is in the failure to recognize that, like other businesses, they must have a cost accounting model that allows them to understand what their cost is for producing the client’s product before they can agree to a sale price.

If you think only manufacturing companies can use cost accounting methods in their businesses, think again. Law firms who are using these methodologies will leave behind those who don’t educate themselves in these practices. You may not be producing widgets, but you are selling a “product” (time) that can be measured in order to determine the cost to produce that product. By implementing a cost accounting system, you will be able to determine profitability by producer, department, office, client, and matter. (You may be surprised to learn that your largest fee income client is not necessarily the largest contributor to your bottom line!)

Determining the Cost of Your Product

So how does a firm determine the cost of their product? It isn’t as complicated as you may think. By determining the direct costs of your timekeepers (salary, payroll taxes, insurance, training, etc.) and allocating the remaining firm overhead to your timekeepers (how the overhead is allocated to differing timekeepers is another article in itself), you can determine an annual cost per timekeeper. By then looking at the number of hours each timekeeper bills per year, you can determine their hourly cost. (Timekeeper annual cost including overhead allocation ÷ number of hours billed = timekeeper cost per hour.)

Once you have determined the timekeeper’s cost per hour, you can readily understand what you can (and cannot) afford to offer as your billable rates and AFAs. You can determine the necessary billable rate for each timekeeper in order to meet your profitability goals, taking into account anticipated write-downs and write-offs (typically 10 percent). You will also know very quickly whether you can afford to offer a client a discount on any given invoice and still receive a profit on that work.

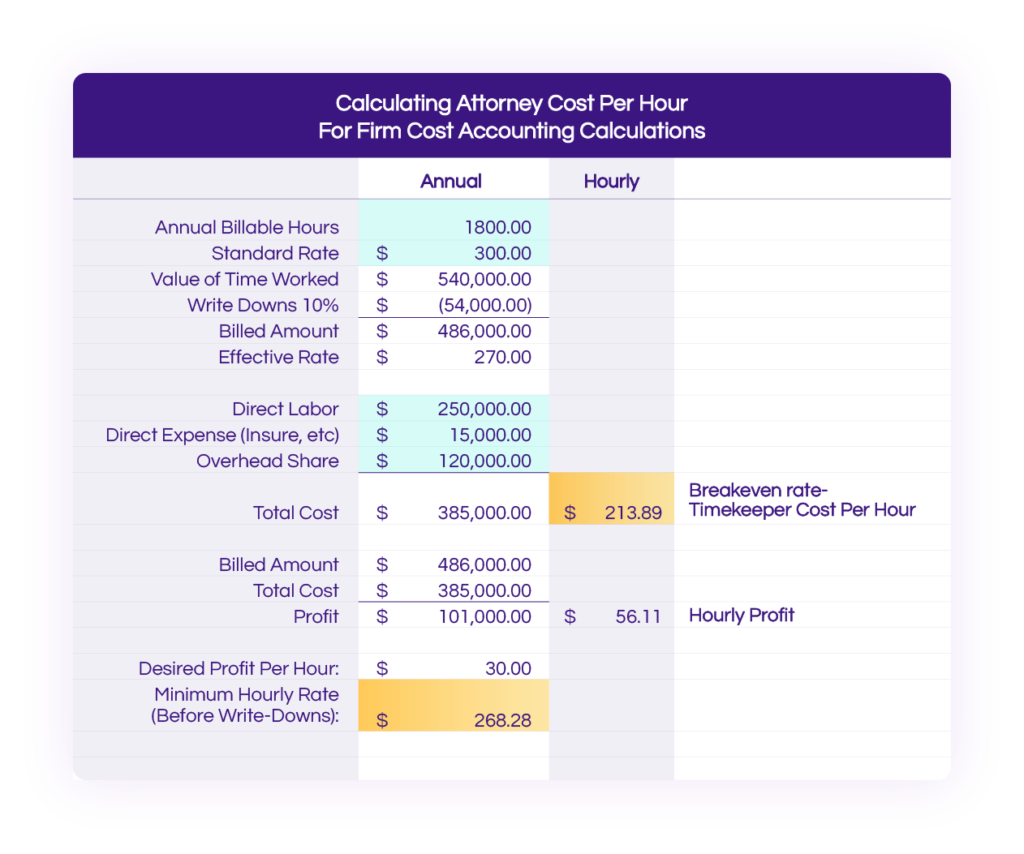

See the example below:

The attorney bills 1800 hours per year at $300 per hour, for a value of $540k.

The sample firm typically sees 10% in write-downs and write-offs, placing the true value of the work at $486k.

This puts the attorney’s effective rate at $270 per hour.

The attorney’s total cost, including their share of the firm overhead, is $385k. At 1800 billable hours per year, this puts their break even rate at $213.89.

What does this spreadsheet tell you?

You need to receive a minimum of $213.89 for each of the attorney’s 1800 billable hours just to break even on this attorney.

At the current hours, rate, and costs, this attorney earns you $56.11 per hour.

If you have a goal of a profit of $30 per hour, the attorney needs to bill a minimum of $268.28 per hour to cover write-downs and write-offs, attorney costs, and get to the desired goal of $30 per hour profit.

How does that help you?

When considering client requests for discounts on their invoices, you know whether you can afford to agree to the client request without losing money.

When considering AFAs, if you know how many hours a project should take you, you can easily come to a flat fee that will meet your desired profitability goals.

When considering whether a client is truly profitable, you know what your baseline number is. Many times our biggest clients expect deep discounts because they “pay us a lot of money.” With this information you can break it down – by looking at who your timekeepers were for an individual client, how much they billed and what their bottom line hourly rate is, you know whether the client is truly profitable to the firm, or whether they are costing you money despite the total amount they spend in fees each year.

By doing a small amount of legwork on the front end to create a model that works for your firm, you can

Ensure you are billing your timekeepers at a rate that will meet your profitability goals;

Look at the profitability of each client based on the timekeepers who have worked on their matter(s) and the effective rates for those timekeepers after receipts;

Be more accurate in your budgeting for client proposals;

Be more competitive by using this knowledge to be creative in your billing models and the use of AFAs.

One final note – be sure to require your attorneys to capture their hours, even on flat fees and other AFA arrangements. If you don’t, you will not be able to determine how successful your AFA models are working for you in helping you to maintain profitability.

Are you ready to manage and grow your firm the way all high-performing practices do?

Grow your firm’s brand and clientele. Enable your staff to hit billable targets painlessly. Then run reports to continuously optimize your firm to reach more profitability. All in one platform.